Top 50 HVACR Distributors of 2019

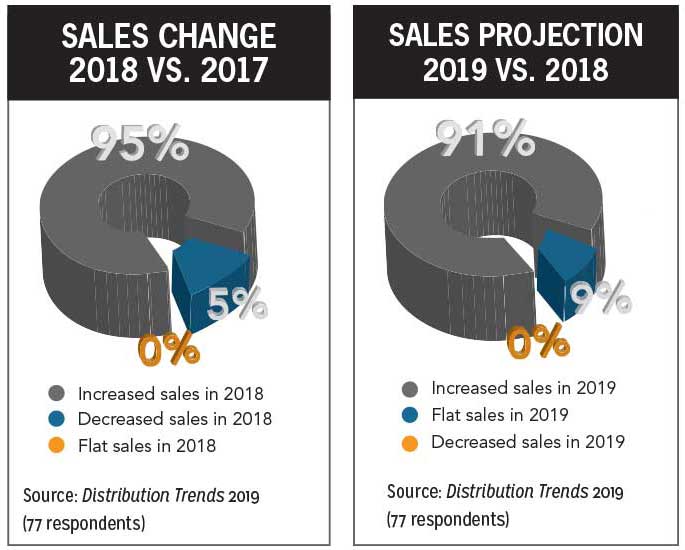

Five years ago, the Top 50 HVACR Distributors survey revealed that 96 percent of respondents had achieved increases in their HVACR sales in the latest fiscal year. This year’s survey nearly matched that phenomenal growth, with 95 percent of all respondents reporting increased HVACR sales.

The outlook for fiscal 2019 is also bright, with 91 percent of all respondents projecting increased sales, and 9 percent expecting to maintain sales at the same level as they did in 2018.

Looking only at the Top 50 companies, every single one showed higher HVACR sales in fiscal 2018 vs. 2017. Thirty-seven of the Top 50 reported double-digit sales increases, and of those, six saw their HVACR sales jump 20 percent or more from the previous year.

AC Pro, Fontana, California, moved up the Top 50 ranking chart from No. 34 in the 2018 survey to No. 26 this year. The company reported a 20 percent-plus increase in sales for 2018, which it attributed to the opening of three new locations in Southern California, additional sales team members, a big push behind its e-commerce/online store, and a focus on quality training for customers and associates.

Others in the Top 50 that achieved 20 percent-plus sales increases in 2018 included Munch’s Supply, New Lenox, Illinois; Hercules Industries, Denver; The Corken Steel Products Co., Florence, Kentucky; American Metals Supply Co., Hazelwood, Missouri; and The Granite Group, Concord, New Hampshire.

Double-digit HVACR sales increases also were reported by the following respondents, which did not appear in the Top 50: First Supply, Madison, Wisconsin; 2-J Supply, Dayton, Ohio; M&A Supply, Brentwood, Tennessee; Dakota Supply Group, Fargo, North Dakota; API of NH, Manchester, New Hampshire; ILLCO Inc., Countryside, Illinois; Team Air Distributing, Nashville, Tennessee; Consumers Pipe & Supply, Fontana, California; Wolff Bros. Supply, Medina, Ohio; C&L Supply, Vinita, Oklahoma; Moore Supply, Lisle, Illinois; Thermosystems, Elmhurst, Illinois; Advanced Filtration Concepts, Norwalk, California; Total Home Supply, Fairfield, New Jersey; and Geothermal Supply, Horse Cave, Kentucky.

Sales Leaders

The same 10 companies have occupied the Top 10 positions on the Top 50 chart for years. The top five companies have remained the same since the Top 50 HVACR Distributors survey was introduced in 2012.

Looking for quick answers on air conditioning, heating and refrigeration topics? Try Ask ACHR NEWS, our new smart AI search tool. Ask ACHR NEWS

Watsco Inc., Miami, has remained No. 1 on the chart for every year of the survey. In 2018, Watsco reported record results for the 2018 fiscal year and also marked its 30-year anniversary in HVACR distribution.

“We’re proud of our track record and industry leadership position, but there is much more for us to achieve in the $35 billion North American HVACR distribution market,” said Albert H. Nahmad, chairman and CEO, Watsco, in a statement. “We continue to challenge Watsco’s leaders to grow, innovate, and build on this success, particularly in light of the cultural and technology evolution underway.”

The company said its record results included 6 percent growth in HVAC equipment (67 percent of sales), 5 percent growth in other HVAC products (29 percent of sales), and flat sales for commercial refrigeration products (4 percent of sales).

Watsco attributed its outstanding performance to continuing technology investments, organizational investments, cultural investments, an enriched wellness program for employees, and continued building of its ownership culture through various unique equity-based programs.

Since 2012, Watsco's technology team has tripled in size, expanding from 60 employees to more than 200. The distributor has added more than 250 customer-facing personnel and functional leaders and recently launched a productivity initiative. Watsco also has increased its annual 401(k) matching contribution.

Ferguson Enterprises (ranked No. 3) reported that of its 1,459 branches/locations, 141 were for HVACR only, 130 were for HVACR and other, and 1,188 were for non-HVACR. R.E. Michel Co. (ranked No. 4) said of its 290 branches/locations, 205 were HVACR only, 78 were HVACR and other, and seven were non-HVACR. Winsupply (ranked No. 6) said that of its 600 branches/locations, 75 were HVACR only, 247 were HVACR and other, and 600 were non-HVACR. F.W. Webb Co. (ranked No. 8) reported that of its 90 branches/locations, 88 were HVACR and other, and two were non-HVACR.

Among all respondents, 53 distributors said they operated HVACR-only branches/locations, 17 said they operated HVACR and other branches/locations, and 78 said they operated non-HVACR branches/locations. Some of those listed above have branches/locations in two or more categories.

| HEATING (AIR)/COOLING TOP 10 | ||

| RANK | COMPANY | % OF HVACR SALES IN THIS SEGMENT |

| 1 | Watsco Inc. | 95% |

| 2 | Johnstone Supply Inc. | 66% |

| 3 | Ferguson Enterprises | 78% |

| 4 | Sigler Wholesale Distributors | 100% |

| 5 | R.E. Michel Co. | 82% |

| 6 | Winsupply Inc. | 80% |

| 7 | Mingledorff's Inc. | 99% |

| 8 | U.S. Airconditioning Distributors | 100% |

| 9 | The Habegger Corp. | 97% |

| 10 | Munch's Supply | 96% |

Total Sales and Other HVACR Industry Data

Based on total HVACR sales for fiscal 2018 reported, the 77 respondents to this year’s Top 50 survey represented $19.1 billion in HVACR sales, which is up 7.9 percent from the $17.7 billion in HVACR sales reported for fiscal year 2017.

Survey respondents were asked if they expected to increase, decrease, or maintain the same number of employees in fiscal 2019. Of the 69 companies that responded to this question, 58 said they planned to increase the number of individuals they employ in 2019, nine said the number of employees would remain the same as in 2018, and two said they were unsure.

Another survey question asked what percentage of HVACR sales were residential and what percentage were commercial. The average was 66 percent for residential HVACR sales and 34 percent for commercial HVACR sales, based on 69 respondents.

| HYDRONIC HEATING TOP 10 | ||

| RANK | COMPANY | % OF HVACR SALES IN THIS SEGMENT |

| 1 | F.W. Webb Co. | 54% |

| 2 | Ferguson Enterprises | 12% |

| 3 | Winsupply Inc. | 15% |

| 4 | Johnstone Supply Inc. | 3% |

| 5 | R.E. Michel Co. | 5% |

| 6 | Sid Harvey's | 25% |

| 7 | Goodin Co. | 45% |

| 8 | First Supply* | 35% |

| 9 | APR Supply | 22% |

| 10 | CCOM Group | 17% |

Changes to the List

Design Air, Kimberly, Wisconsin; Minnesota Air, Bloomington, Minnesota; and The Granite Group, Concord, New Hampshire, are all new companies in this year's Top 50 ranking.

Design Air is a full-service HVAC wholesale distributor serving licensed HVAC contractors in all of Wisconsin, upper Michigan, eastern Minnesota, and northern Illinois.

Minnesota Air is a family-owned business that started out as an independent plumbing wholesaler in the U.S. in the early 1950s. In 1981, Minnesota Air was created as a wholly owned subsidiary of that company. In 1999, it became a separate corporation, distributing equipment, parts, and supplies to HVACR contractors in Minnesota, eastern North Dakota, and western Wisconsin.

The Granite Group is a full-service wholesale distributor of plumbing, heating, cooling, water, and propane supplies, serving all of New England.

| REFRIGERATION TOP 10 | ||

| RANK | COMPANY | % OF HVACR SALES IN THIS SEGMENT |

| 1 | Johnstone Supply | 10% |

| 2 | Watsco Inc. | 5% |

| 3 | American Refrigeration Supplies | 50% |

| 4 | ABCO HVACR Supply + Solutions | 24% |

| 5 | Gustave A. Larson Co. | 19% |

| 6 | F.W. Webb Co. | 11% |

| 7 | Sid Harvey's | 21% |

| 8 | Ferguson Enterprises | 2% |

| 9 | Young Supply Co. | 2% |

| 10 | Meier Supply Co.* | 50% |

Industry Outlook and Observations

Survey respondents were invited to comment on the factors they expect will most impact HVACR distribution in 2019. More than 30 respondents shared their views, but most preferred to comment anonymously. They listed the economy, housing, tariffs, inflation, new locations, residential growth, e-commerce, consumer confidence, price increases, government regulations, efficiency requirements, freight cost, interest rates, human resources, finding labor, rising labor rates, a shortage of truck drivers, and online sales pressures among their largest challenges.

Carlton Harwood, vice president of HVAC at Ferguson, cited the following as factors he expects to impact HVACR distribution: product availability and pricing; growth in digital and omni-channel; growth in ductless, VRF, and high-efficiency, forced-air products; growth in connected home products; labor scarcity for tradesmen and drivers; and contractor business solutions (i.e. financing, product support, etc.).

Tim Brooks, president of Lohmiller & Co., dba Carrier West (No. 25), is concerned about finding qualified workers.

“Labor shortages will continue to put additional pressure on distributors and contractors,” he said. “Price increases will also continue to be a challenge in the overall cost of new construction and replacement markets. Additionally, the new fan efficiency ratings requirement this July will require a lot of education for consumers and builders alike. The new standard comes with increased cost but will greatly reduce energy consumption in homes and commercial buildings.”

| WHAT PERCENTAGE OF YOUR BUSINESS IS COMMERCIAL? | |

| NUMBER OF RESPONDING COMPANIES | % RANGE FOR COMMERCIAL BUSINESSES |

| 7 | 80% to 100% |

| 10 | 50% to 79% |

| 20 | 30% to 49% |

| 27 | 10% to 29% |

| 5 | 1% to 9% |

| Overall average | 34% |

Matt Bedard, CEO, S.G. Torrice Co. (No. 47), Wilmington, Massachusetts, said distributors cannot underestimate the Amazon effect.

“Distributors need to differentiate their ability to help customers maintain their relevance by leveraging digital marketing efforts and social media outlets,” he said. “We're also seeing an increased level of sales initiated via our online shopping experience.”

Bedard also noted that changes in high-efficiency rebates will have an impact on product mix.

“The anticipated softening of the new construction market will also impact the industry,” he said.

Stephen Torrice, president and owner, S.G. Torrice Co., said his region is still recovering from the last economic downturn.

“Concerns include single-family construction, which is affected by interest rates, among other things; availability of an adequately trained workforce; and the simple fact that this recovery has been going on eight years,” he said. “That's a longer than average recovery.”

Devin Watts, treasurer, M&A Supply Co., Brentwood, Tennessee (No. 54), a distributor of residential and light commercial HVAC equipment and supplies, said the performance of the economy will continue to be a significant factor.

“The economy, trade issues, and tariffs impact the amount of disposable income consumers have to spend, which will drive the market,” he said. “Will costs rise to a point where the replace versus repair issues arise? Do consumers have enough disposable income to continue to replace the backlog of systems in the installed base that need to be replaced?"

Like many of his peers, Peter Warren, CEO, Benoist Brothers Supply Co., Mount Vernon, Illinois (No. 55), a full-service wholesaler distributor of heating and air conditioning products, cited the economy, price increases, and labor availability as his most pressing concerns.

| WHAT PERCENTAGE OF YOUR BUSINESS IS RESIDENTIAL? | |

| NUMBER OF RESPONDING COMPANIES | % RANGE FOR RESIDENTIAL BUSINESSES |

| 17 | 81% to 95% |

| 31 | 60% to 80% |

| 14 | 40% to 59% |

| 2 | 30% to 39% |

| 5 | 1% to 29% |

| Overall average | 66% |

James Luce, CEO/owner, Luce, Schwab & Kase Inc., Fairfield, New Jersey (No. 57), said rising interest rates could slow residential sales.

“We expect the commercial market to stay strong in the New York metropolitan area, as building owners continue to exercise Section 179 of the tax code, which allows for immediate depreciation of new HVAC systems,” he said.

Kevin Parsley, vice president, ACR Supply Co., Durham, North Carolina (No. 66), believes general economic trends are moving in the right direction.

“The trends are positive, and we believe 2019 will have significant growth opportunities for distributors who are positioned correctly,” he said. “We see engineered products, projects — both plan spec and design build — as opportunities for significant growth. We're also seeing nice increases in our B2B e-commerce platform. Large commercial refrigeration projects are increasing as well.”

Teri Moyer, CMO, Advanced Filtration Concepts (No. 71), Norwalk, California, cited government and state regulations regarding air filtration and IAQ as well as tariffs as factors that will impact HVACR distribution.

Mike Luongo, president, Total Home Supply (No. 73), a wholesaler/distributor based in Fairfield, New Jersey, expects ductless sales to continue to soar.

“We anticipate our growth to come from the multi-zone ductless mini-split category,” he said. “This category has been growing year after year.”

Publication date: 4/15/2019

Want more HVAC industry news and information? Join The NEWS on Facebook, Twitter, and LinkedIn today!

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!