Top 50 HVACR Distributors of 2016

For the fifth consecutive year, the movers and shakers among US HVACR wholesalers reported sales growth and a positive outlook.

Total HVACR sales represented by the Top 50 Distributors each year have steadily increased. In 2012, they accounted for more than $10.3 billion (fiscal year 2011); this rose to more than $11.5 billion in 2013, $12.8 billion in 2014, and $13.8 billion in 2015. This year, the top 50 represented $14.8 billion in sales for fiscal 2015.

Total HVACR sales represented by the Top 50 Distributors each year have steadily increased. In 2012, they accounted for more than $10.3 billion (fiscal year 2011); this rose to more than $11.5 billion in 2013, $12.8 billion in 2014, and $13.8 billion in 2015. This year, the top 50 represented $14.8 billion in sales for fiscal 2015.

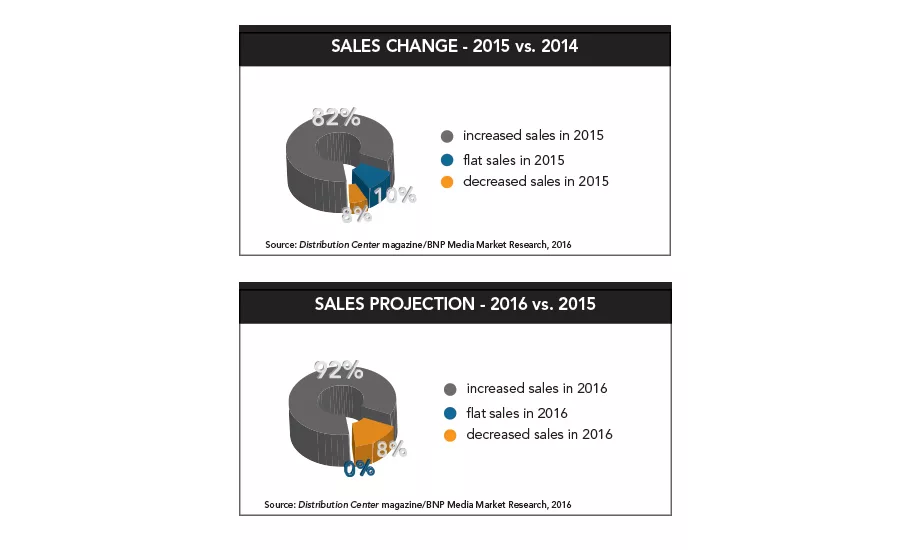

When Distribution Center and the Heating, Air-conditioning, and Refrigeration Distributors International (HARDI) introduced the Top 50 HVACR Distributors survey in May 2012, 80 percent of respondents reported a rise in HVACR sales in fiscal year 2011 versus 2010. In May 2013, 78 percent of the Top 50 reported higher HVACR sales; this increased to 96 percent with higher sales in May 2014 and 75 percent in the May 2015 survey. The 2016 study found that 82 percent of the top 50 enjoyed higher HVACR sales in fiscal year 2015, with an average increase of 7.9 percent.

The monthly TRENDS report by HARDI indicated 5.7 percent annualized growth for the 12 months through December 2015.

Among the Top 50 on this year’s list, 94 percent are HARDI members. Affiliated Distributors (AD) HVAC Division has 30 members with 573 locations and annual HVAC sales of more than $3.2 billion, according to AD.

Sales projections for the Top 50 have also risen over the years. Seventy-nine percent predicted a sales increase in 2012, 87 percent in 2013, 91 percent in 2014, and 89 percent in 2015; this year, 92 percent said they expect higher sales in 2016.

The 2016 Top 50 study received responses from 61 distributors, of which 77 percent had increased HVACR sales in 2015 with the average being 8.2 percent higher than 2014. Also, 11 percent reported flat sales, and 11 percent had lower sales with an average decrease of 6.5 percent.

Among the 61 survey respondents’ projections for 2016, 90 percent predicted a sales increase, up on average 8.8 percent; 2 percent predicted flat sales;, and 8 percent predicted a decrease in sales of 2 percent. Of the 61 responding companies this year, 92 percent are HARDI members.

Looking for quick answers on air conditioning, heating and refrigeration topics? Try Ask ACHR NEWS, our new smart AI search tool. Ask ACHR NEWS

Sales Stars

Among the Top 50, 14 distributors reported double-digit sales increases for fiscal 2015: Ferguson, Sigler Wholesale, Winsupply (formerly WinWholesale), US Air Conditioning Distributors, Slakey Brothers, Century Holdings, Value Added Distributors, Munch’s Supply, Lohmiller & Co., Shearer Supply, AC Pro, Corken Steel Products, Young Supply and Robertson Heating Supply.

Winsupply and Climatic Comfort Products, a seven-branch HVACR distributor based in Columbia, South Carolina, both reported sales increases of 20 percent or more in 2015.

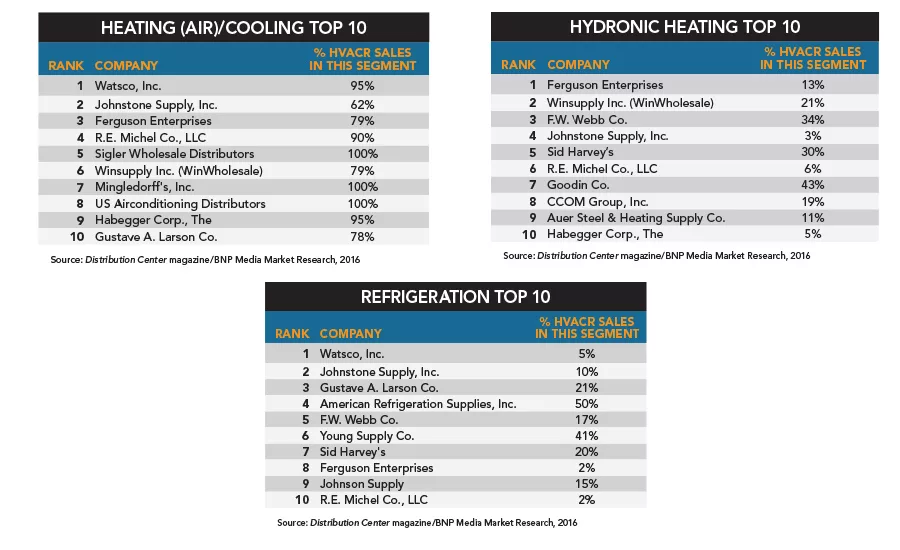

Among the survey respondents that projected double-digit increases in HVACR sales for 2016 were Ferguson Enterprises, US Air Conditioning Distributors, F.W. Webb, Shearer Supply, Munch’s Supply, Century Holdings and AC Pro. United Supply Co., North Plainfield, New Jersey, which was not on the list but ranked at No. 58 this year, with nine locations, projected a 10 percent sales increase for 2016. United Supply said 80 percent of its total sales are in HVACR with 85 percent of its HVACR sales being in heating (air)/cooling equipment and supplies and 15 percent in hydronic heating.

The No. 1-ranked distributor this year, Watsco, reported sales growth of 4 percent in 2015 (5 percent on a same-store basis). The company said its sales of HVAC equipment grew 7 percent, including 8 percent growth in the U.S.; its sales of other HVAC products grew 2 percent, and its sales of commercial refrigeration products also increased by 2 percent.

In January 2016, Watsco named Aaron J. Nahmad its president. He had served as vice president of Strategy & Innovation at Watsco since July 2010 and led the company’s transformation into the digital age. He is the son of Albert Nahmad, who has been serving as chairman, president and CEO of Watsco since 1973.

No. 2-ranked distributor Johnstone Supply describes itself as the top cooperative wholesale HVACR distributor in the country. It operates a six-point distribution network with centers in Portland, Oregon; Las Vegas; Dallas; Joliet, Illinois; Allentown, Pennsylvania; and Jacksonville, Florida.

Today, Johnstone says its 400 locations across the U.S. have sales and growth that continue to outpace the industry average. The company’s President and CEO is DeWight Wallace, who supports technology and eCommerce as part of a progressive company vision and strategic plan.

Ferguson Enterprises, ranked No. 3, has 1,400 locations and says 10 percent of its total company sales are in HVACR. Ian Meakins, chief executive at Wolseley plc, parent company of Ferguson, said in a statement that “continued good growth” is expected in the U.S. in HVAC, as well as other categories, such as waterworks and fire and fabrication.

“From the perspective of the overall economy, there are plenty of positives supporting HVACR distribution,” said Alex Hutcherson, vice president – HVAC at Ferguson Enterprises. “Residential construction remains steady, and nonresidential construction is rebounding, giving 2016 the potential of being a milestone year for the HVAC industry. Beyond the overall economy, emerging technologies and trends, like ductless and VRF systems, continue to increase in popularity and will make up more of the market. Distributors will be increasingly challenged to stay ahead of the curve when it comes to supporting HVAC contractors and service technicians in charge of installing these products,” Hutcherson said.

Company Close-ups

Two companies on the Top 50 ranking chart are using different names this year.

WinWholesale, ranked No. 6 in the 2015 study, is ranked No. 6 again in 2016, but as Winsupply. WinWholesale changed its name to Winsupply Inc. in September 2015 in response to “the utility and attractiveness of the Winsupply brand, its recognition in local markets and its acceptance by local wholesalers, customers, and vendors,” the company said in a press release.

“This name change supports our desire to create a cohesive, powerful brand —Winsupply —that aligns with the changing marketplace, enhances the customer experience, strengthens the local companies, and delivers more value to all of the shareholders throughout the Win family of companies.”

Morrison Supply Co., ranked No. 19 in the 2015 study, appears on this year’s chart at No. 18 as Morsco. Morrison Supply had sold majority shares to Advent International in November 2011, which led to the inception of Morsco, a private company sponsored by Advent International and led by a team of industry veterans, including Chip Hornsby. Morsco is a leading U.S. distributor of commercial and residential plumbing, HVAC, and PVF, and it has grown rapidly through acquisitions and store openings. In September 2015, Morsco acquired Murray Supply and announced it now comprises seven business operating units: Morrison Supply, Express Pipe & Supply, Farnsworth Wholesale, Wholesale Specialties, Expressions Home Gallery, Kiva Kitchen & Bath and Murray Supply.

Famous Enterprises, ranked No. 25 this year, generates 40 percent of total company sales from HVACR, according to Marc Blaushild, president and CEO. Plumbing and PVF represent another 40 percent of total company sales. The remaining 20 percent is evenly split with 10 percent each for industrial products and building products. The company has seen growth in building products in the past year, Blaushild said.

American Import and Export in San German, Puerto Rico, has 12 locations and 130 employees. American Import and Export in San German, Puerto Rico, has 12 locations and 130 employees. Ranked No. 59 this year, the company said 52 percent of its total sales are in HVACR and the breakdown is: 50 percent heating (air)/cooling; 20 percent hydronic heating, and 30 percent refrigeration.

Ranking Changes

Several other companies changed position in the rankings this year, as well. Slakey Brothers moved from No. 21 in the 2015 chart to No. 17 this year. Century Holdings moved from No. 25 in 2015 to No. 21 in 2016. Coburn Supply moved from No. 36 in 2015 to No. 32. Shearer Supply moved from No. 40 to No. 37. Goodin Co. moved from No. 47 to No. 43 in 2016. American Metals Supply, Hazelwood, Missouri, with seven locations, moved from No. 51 in 2015 to No. 50 on the 2016 chart. Acme Refrigeration of Baton Rouge, Louisiana, which was No. 58 last year, moved up to No. 53 in 2016. Acme Refrigeration reported a 13 percent sales increase in fiscal 2015. The company says 99 percent of its sales are in HVACR with 90 percent in the heating (air)/cooling equipment and supplies and 10 percent in refrigeration.

A few companies lost their place on the list this year, including Williams Distributing, which dropped from No. 50 in 2015 to No. 51 this year; and The Granite Group, which dropped from No. 45 in 2015 to No. 52 this year.

Sales Breakdowns

This year’s survey found that 43 of the Top 50 distributors generated 50 percent or more of total company sales from HVACR. Also, 35 of the Top 50 said 90 percent or more of their total company sales were in HVACR.

The breakdown by segment within HVACR was:

• 83 percent in heating (air)/cooling equipment and supplies.

• 4 percent hydronic heating.

• 5 percent refrigeration.

• 8 percent other.

Included in “other” were: ancillary products, controls, tools, metal, pipe, sheet metal, motors, propane-related products, VRF, parts and pieces.

Respondents’ Comments

Here are some responses Distribution Center received to the survey question, “What factors do you expect to most affect HVACR distribution in 2016?”

- “The general economy in the markets we serve, government (both federal and local) policies and regulations.”

-Lanny Sigler, vice president, Sigler Wholesale Distributors

- “We will be opening new outlets to better service our customers.”

-John Scarsi, vice president/chief financial officer, US Air Conditioning Distributors

- “Regional standards and R-22 phaseout.”

-Ryder Horky, vice president/general manager, Insco Distributing Inc.

- “[The] economy and legislation.”

-Claire Munch, director, customer service, Munch’s Supply LCC

- “DOE and EPA regulation.”

-Douglas Wight, vice president – sales and marketing, Refrigeration Sales Corp.

- “Efficiency increases of products used in HVAC systems, commercial and residential.”

-Gene Boos, senior vice president, S.W. Anderson Sales Corp.

- “Growth of new construction in our territory.”

-Jay McDaniel, president/CEO, Team Air Distributing Inc.

Other comments by respondents who asked not to be named included:

- “Expected improvement in economy in the second half of the year.”

- “Tight supply of R-22. Stranded 13-SEER inventory in the southern regions. Outcome of import-duty decision on Chinese refrigerants. More production being moved to Mexico.”

The most frequently cited factors by those who asked for anonymity were the economy and regulation/legislation, rebates/credit/prices, the weather and the R-22 phaseout and subsequent stranded 13-SEER inventory. Other factors mentioned included succession planning, new products and retaining talent.

This year’s survey also invited comments on anything related to the HVACR industry. Here are some responses we received:

- “Energy-efficiency standards could become so stringent and make our products so expensive that many people will no longer be able to afford them.”

-Lanny Sigler, vice president, Sigler Wholesale Distributors

- “With its continued phaseout, it will be interesting to see where the dollar threshold will be for contractors to move from R-22 to an alternative.”

-Ryder Horky, vice president/general manager, Insco Distributing

- “Competition continues to be the main issue.”

-Gene Boos, senior vice president, S.W. Anderson Sales Corp.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!