Forecasting The Economic Climate

ATLANTIC CITY, NJ — Last year’s hvac business started in a hole. Contractors knew it. Wholesalers knew it. Manufacturers knew it. Most had started bracing for a recession based on downward trends months before the economic analysts stamped that recession a fact.

Then came the tragedies of Sept. 11. In the midst of the economic aftermath affecting the travel, retail, and entertainment industries, we all wondered how the hvac industry would fare.

Now, as the industry gathers here in Atlantic City for the 2002 International Air-Conditioning, Heating, Refrigerating Expo, the numbers for the end of last year have started to solidify.

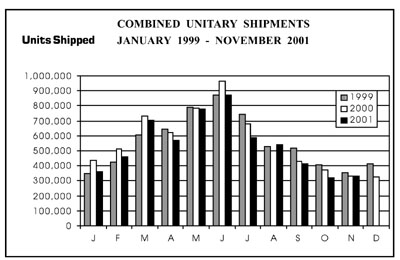

The news is good in that it could have been a lot worse. Through November 2001, total unitary shipments were down 6% from 2000, according to the Air-Conditioning and Refrigeration Institute (ARI). That’s up a percentage point from October — and some manufacturers speculated that, by year’s end, that figure would wind up around 5% off 2000’s numbers.

According to the latest ARI figures (through November 2001), combined U.S. factory shipments of 333,414 central air conditioners and air-source heat pumps were up 1% compared to shipments from November 2000. Heat pump shipments, at 96,695, were up 9% over last November’s figure.

Considering that the year started with shipments off in double-digit percentages from January 2000, and combined with the blow dealt to the economy and national security on September 11, this is news to be thankful for.

2001 BY THE NUMBERS

In January 2001, ARI reported that “Combined U.S. factory shipments of 358,555 central air conditioners and air-source heat pumps for January were down 17% compared to shipments from the same month last year. Heat pump shipments of 91,611 were down 3%, compared to January 2000.”By June, “Combined U.S. factory shipments of 873,558 central air conditioners and air-source heat pumps fell 9% below the June 2000 record of 963,429 units,” the institute reported. Heat pump shipments, moreover, jumped 5% above June 2000. Combined shipments for the first six months were 8% off 2000’s figures.

Matt Peterson, vice president of sales and marketing for York, said these reports and others have the company “cautiously optimistic; 2000 was flat over 1999; 2001 is going to end up down about 8%. That’s where the figures were through August, and they haven’t changed significantly from that in October and November.”

Looking for quick answers on air conditioning, heating and refrigeration topics? Try Ask ACHR NEWS, our new smart AI search tool. Ask ACHR NEWS

Jon Shaw, senior manager of communication and PR for Carrier/UTC, conceded a weakness in North American hvac, and a reluctance in consumers to spend on new projects. However, “We’ve been seeing that reluctance all year long.” It started long before September 11 with what Shaw called the “NASDAQ disintegration.”

Lennox’s Doug Young noted that for the North American residential market, 2001 started off “in a hole. We’re now down to roughly 5.1%.” Young is vice president and general manager for the manufacturer’s North American residential sales, marketing, and distribution.

“Every segment with the exception of heat pumps is down,” he continued. Driving factors for that market, Young said, include the fact that the heat pump’s dominant region, the Sunbelt, still has strong new construction work.

Contractors have been conducting business conservatively this last year, Young said. “The draw down of inventory has been steady throughout the year,” depleting what had been a build up of inventory in the pipeline.

THE EFFECTS OF 9-11

All U.S. business came close to a standstill in the days immediately following September 11. Added to the shock were complications stemming from travel restrictions and great general uncertainty. How would consumers respond?Thankfully, since September 11, the hvac industry has been running as it had been year to date. ARI’s October figures put it down 7%, Peterson noted.

Winter so far has been soft, he added, and furnaces have remained flat. This is mainly due to unseasonably warm weather.

Carrier’s Shaw said that in the aftermath of September 11, “The good news was that we didn’t lose any orders. The bad news is, we didn’t have any orders” relative to other years.

Consumer attitudes also came through fairly well. In fact, as far as purchases for home comfort go, “The cocooning effect is alive and well,” said Lennox’s Young.

Unemployment has reached short-term record highs, he continued. This can affect durable goods purchases. Third-party reports have centered around a recession, “tough times,” and intensification of a lean, competitive market, said Young. Under these conditions, the consumer purchase process for durable goods takes longer, he said.

WHAT 2002 HAS IN STORE

In 2002, “Expect business to be flat,” down by 5%, said York’s Peterson. Housing starts have been flat to slightly down, he said. “Interest rates should keep housing starts flat.” Manufactured housing, which helped offset the down business in the second half of 2001, should carry its positive effects over into 2002, he said.“Our optimistic scenario is the residential market, especially residential replacements,” he continued. Replacements should be buoyed by last year’s light summer, Peterson explained; it didn’t get hot until late in the season, so people put off replacing their units. Therefore, contractors can expect spring replacements to get a boost, especially if the weather cooperates.

“Air conditioning in summertime is now a necessity,” he pointed out. If a homeowner had central air before, they are highly likely to replace it with another central system. They will not go back to room units if they can help it.

Then there’s that cocooning trend, which will probably get a boost due to general feelings of insecurity. Futurist author Faith Popcorn, in her 2002 report (which was released Dec. 19, 2001), points to “the armored cocoon,” complete with filtered air and water, “for those who crave protection in an uncertain world.” (Popcorn is a best-selling author of and founder of BrainReserve, a futurist marketing consultancy she established in 1974.)

The commercial side will probably be more unstable than the residential, noted Peterson. Spending has been, and will continue to be, conservative for shopping centers, strip malls, and office buildings.

Shaw, Peterson, and Young each noted that for 2002, industry shouldn’t expect to see significant economic improvements until roughly mid-year. That means among all market segments, now is the time to tighten belts and work toward greater business efficiency.

“What doesn’t kill you, makes you stronger,” pointed out Shaw. “What worked yesterday won’t necessarily work today.”

THE CONTRACTING MARKET

Contractors can expect a much more competitive market, of which they’ve probably already gotten a taste. “There will be a fallout of less-qualified businesses,” Peterson predicted.To improve their odds of survival, “Contractors have got to diversify,” he continued. “Make sure you focus on all the segments you can.” Cultivate more commercial and residential service and maintenance agreements. And if you can, get into controls.

“In this business, success means having a fundamentally qualified business,” Peterson said. “When business was booming, some people were making money and they didn’t know why.”

Companies will have to work harder to stay busy, he continued. “The replacement sales are still there — but contractors and their staffs may have to work harder to educate owners on the benefits of replacing rather than repairing.”

This winter’s weather, or early lack thereof, has been troubling for hvac companies, Young said. However, it’s good news for consumers; it puts money in their pockets for durable goods, like a/c.

Still, “If they don’t have to replace it, they won’t,” Young said. They will need guidance on the benefits of a new system.

“Contractors are saying there is plenty of service work,” Young continued. “It’s been constant. They clearly want a steady flow of replacements.

“Consumers are attracted to known and trusted brands,” he said. “Our dealers are doing a very good job of marketing, and targeting consumers who are ready to pay for durable goods purchases.”

The biggest mistake a company could make, he said, is that “In tough times, people start cutting ad and marketing funds. Opportunities then fall at a faster rate.”

Publication date: 01/14/2002

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!