Buy Now, Pay Later Grows as Option for Funding HVAC Repairs, Replacements

Finance options draws more interest from consumers, regulators

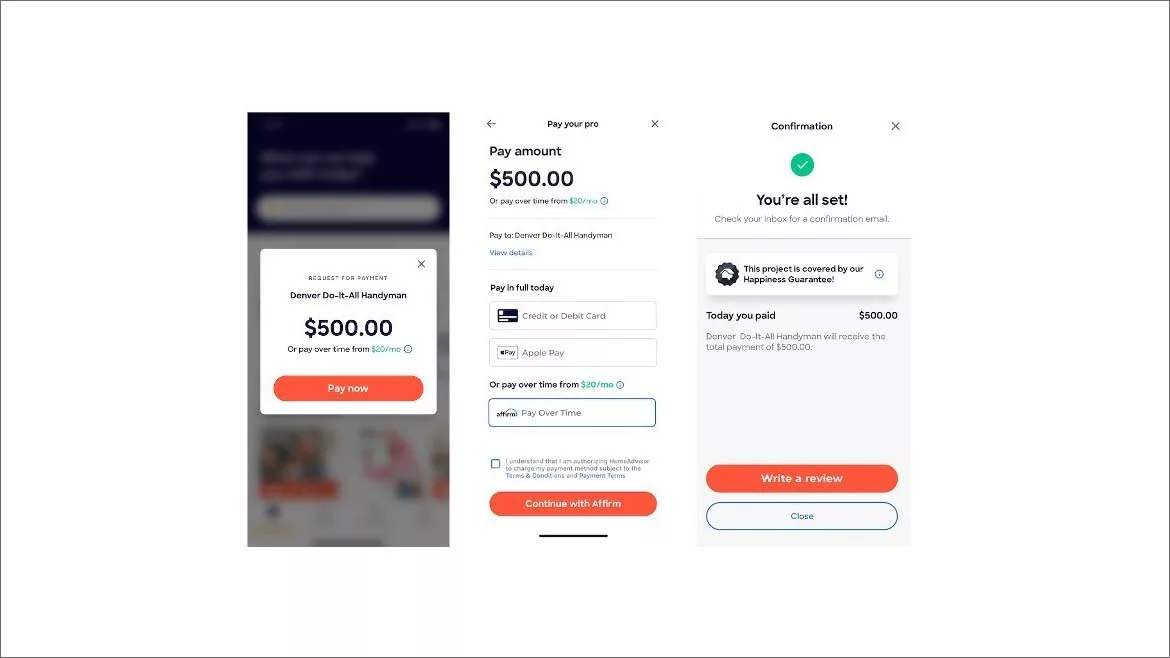

ANOTHER OPTION: Consumers paying for an HVAC project via the HomeAdvsior app now have the option to use a buy now, pay later program from Affirm. (Courtesy of PR Newswire)

Buy now, pay later, known better as BNPL, is the hottest trend in finance these days. Consumers are using this method to purchase everything from Christmas gifts to airline tickets. Some are even using it to pay for HVAC work.

So how does it work? These are essentially point of sale retail installment plans. Consumers make a down payment, usually 25%, and then make further payments over a set period of time. It’s similar to layaway, except the consumer receives their purchase upfront. It’s also essentially the way homes and cars have been financed for decades.

BNPL providers require little information to approve the financing, so it appeals to consumers with either little credit history or damaged credit history. The buyer must make the agreed-upon payments at scheduled times. There is often no interest or fee charged, but there is also no avoiding or reducing the scheduled payments.

Merchants pay between 3% and 6% of the sales amount to the finance provider. They are, in turn, paid in full for the product or service, and the settlement of the debt is between the BNPL firm and the consumer.

HomeAdvisor Partners with Affirm

This type of financing has been available for some HVAC contractors for more than a year. HomeAdvisor partnered with BNPL provider Affirm in December 2020. This was the first such partnership between a home services platform and Affirm.

Homeowners using the HomeAdvisor Pay option on the company’s app can select Affirm at checkout. HomeAdvisor customers can also use Affirm at checkout for its instant pre-priced projects as well as any managed project.

Consumers can select term lengths ranging from three to 36 months. For example, a $5,000 project would cost $452 per month over 12 months with 15% APR. Affirm is one of the BNPL providers that does charge interest.

Looking for quick answers on air conditioning, heating and refrigeration topics? Try Ask ACHR NEWS, our new smart AI search tool. Ask ACHR NEWS

“Payment is a particularly stressful part of the home services experience, be it due to unexpected expenses or the lack of transparency around the cost of many home improvement projects,” said Brandon Ridenour, CEO of HomeAdvisor parent Angi, in a December 2020 release.

Director, Consumer Financial Protection Bureau

Federal Regulator Expresses Concerns

As consumer use of BNPL grows, so does the interest of regulators. The Consumer Financial Protection Bureau recently issued orders to five BNPL companies to collect information on the risks and benefits about the type of financing they offer. Affirm is one of the five.

“Buy now, pay later is the new version of the old layaway plan, but with modern, faster twists where the consumer gets the product immediately but gets the debt immediately too,” said CFPB Director Rohit Chopra.

One concern of CFPB regulators is that the apps make BNPL the preferred payment option of consumers. Unlike a credit card account, each BNPL-financed purchase is a separate transaction. This creates multiple due dates, increasing the likelihood that a consumer either forgets to make a payment or lacks the funds to do so.

In addition, protections that apply to credit cards may not apply to BNPL products. Many BNPL companies do not provide dispute resolution protections available to users of other forms of credit, like credit cards.

CFPB regulators also expressed concern about the lack of consistency among the practices of BNPL providers. For example, some BNPL products do not provide certain disclosures, which could be required by some laws. Depending on what rules the lender is following, different late fees and policies apply.

Finally, since BNPL is mainly a fintech product, CFPB regulators are looking at the way these companies harvest consumer data. The CFPB announcement about the inquiry states that some BNPL providers “have used this collected data to create closed loop shopping apps with partner merchants, pushing specific brands and products.”

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!