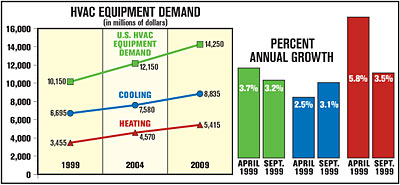

U.S. HVAC Equipment Demand May Reach $14.3 Billion in 2009

"Beyond simply replacing heating and cooling units that are no longer functional, energy efficiency is the primary factor driving sales in the replacement market since newer units have much lower operating costs, in terms of maintenance requirements and energy usage, than older units," said Freedonia analyst Jennifer Mapes.

According to the study, the demand for HVAC replacements and improvements comprise about 70 percent of total demand. Growth in the replacement sector will benefit from increasing interest in more energy-efficient building systems, driving the replacement of older HVAC equipment.

HVAC shipments are forecast to advance somewhat slower than demand, at 2.7 percent per year to $12.9 billion in 2009, as import growth from Asia continues and exports stagnate.

GROWTH AREAS

The study also showed that the market for equipment like heat pumps will grow substantially because of the ability of heat pumps to provide efficient heating and cooling in moderate climates, and to serve as a low-cost, supplementary heat source in colder climates.Packaged terminal air conditioners and chillers are forecast to achieve above-average annual gains, benefiting from their use in industrial and commercial markets, two areas that are expected to post strong recoveries in construction spending through 2009.

Mapes also addressed growth possibilities in niche markets such as geothermal, solar, and wind energy-based systems.

"We are forecasting geothermal heat pumps to grow from its small base, but at a relatively modest rate since growth is restrained by the much higher initial costs of a geothermal heat pump relative to other competitive heating and cooling units," she said.

"Solar and wind are extremely niche technologies still, so they are not expected to have much of an impact on the HVAC industry in the aggregate in the near term. The impact of solar and wind systems is more likely to be felt well beyond our five- and 10-year forecast periods."

Looking for quick answers on air conditioning, heating and refrigeration topics? Try Ask ACHR NEWS, our new smart AI search tool. Ask ACHR NEWS

She noted that gas and electricity will continue to be the dominant technologies for the foreseeable future because the vast majority of buildings are configured to support these technologies. A change would require a significant investment.

FACTORS AFFECTING GROWTH

The new 13 SEER standard will play an important role in the residential replacement market, said Mapes. She said that initially the change in the minimum efficiency would have a negative impact on equipment sales."In the near term, this change will restrain unit gains because consumers may be deterred from purchasing new units because of the higher cost," she said.

"Additionally, many consumers purchased a unit before their dealer ran out of stock of the units built under the previous standard. However, that effect is likely to smooth out by the end of our five-year forecast period, with trends returning to more normal levels."

Energy prices continue to play a key role in consumers' buying decisions. The recent spikes in natural gas prices and anticipated increase in electricity rates have consumers shopping for the most energy-efficient equipment. But those aren't the only reasons for sending consumers on a shopping spree.

"The factors that are more likely to affect U.S. energy prices over the five- to 10-year forecast periods are more likely to be insufficient refining capacity or a supply disruption similar to that which occurred during the past Gulf hurricane season," said Mapes.

She does not see China's impact on the supply of natural resources as having a dramatic influence on the U.S. energy market, and subsequently, on HVAC equipment manufacturers and contractors. "China's impact will be largely in oil, which is not as widely used for heating and cooling in the United States as other types of energy."

Mapes cited a recent article in The Wall Street Journal, in which the author discussed how the Chinese are backing out of natural gas contracts and are going to have to start using coal on a larger level again for power generation. "It seems that the Chinese will have a greater impact on demand for oil than for natural gas in the coming years," she concluded.

FORECASTING FURTHER OUT

Looking further down the road, Mapes said she doesn't see the phaseout of HCFC-22 as having an immediate impact on the market immediately following 2010. "Much of the impact on the replacement market will be felt beyond our forecast periods," she said. "The impact on the replacement market itself tends to be slow, even when the refrigerant is banned."She cited a recent example. "An EPA rule banned the U.S. production of Class I CFCs in 1996, but less than 60 percent of the CFC-based cooling systems were replaced within 10 years. Additionally, because of the high cost of replacement, many building owners have delayed replacement (until they need to for mechanical or efficiency reasons) because the units are allowed to remain in operation and the units can still be serviced, although that service is heavily regulated and increasingly expensive because of their use of a banned refrigerant."

The study concluded that advances in HVAC equipment demand will be spurred by growth in the nonresidential market, which accounted for 60 percent of sales value in 2004. Increases in the nonresidential market will be driven by a projected rebound in nonresidential construction, but further gains will be restrained by the prevalence of reconditioned HVAC systems in this market.

Contact Corinne Gangloff of The Freedonia Group at 440-684-9600 or e-mail pr@freedoniagroup.com to purchase HVAC Equipment (published December 2005, 267 pages). For more information, visit www.freedoniagroup.com.

Publication date: 03/20/2006

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!