2009 Residential Unitary Market Trends

Figure 1.

Contractors responding to this survey reported an annual sales average of $2 million, with 60 percent coming from the sales of residential heating/cooling equipment.

Responding contractors sell an average of three brands, and intend to do so five years from now. Although contractors expect the number of brands available to decline by approximately one-third in the next five years, the number of brands available has remained fairly consistent during the past six years. The presence of import manufacturers is expected to increase during the next five years.

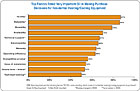

When deciding which brand of residential unitary equipment to purchase, quality, reliability, and durability are “very important” factors followed by availability, technical support, serviceability, warranty, and operating efficiency. The importance of warranty, operating efficiency, competitive pricing, distributor credit, and rebates/incentives has increased significantly since 2007. (See Fig. 1.)

Figure 2.

Almost one in four indicate that their customers always rely on them to decide which brand they purchase. The likelihood of a customer calling a company because of a brand carried has increased significantly during the past two years. (See Fig. 2.)

Figure 3.

For more information about the 2009 Residential Unitary CLEAReport, please contact Jennifer Loomis at loomisj@clearseasresearch.com or 248-786-1630, or Beth Surowiec at surowiecb@clearseasresearch.com or 248-786-1619. The full report includes brand familiarity, product quality, brands purchased, top three industry leaders in five years, brand satisfaction ratings for 52 brands, and important factors driving brand purchase decisions.

Publication date: 10/12/2009

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!