HVAC Production Persists Despite Covid-19-Related Losses

Quarterly earnings show decline; new construction likely to take a temporary hit

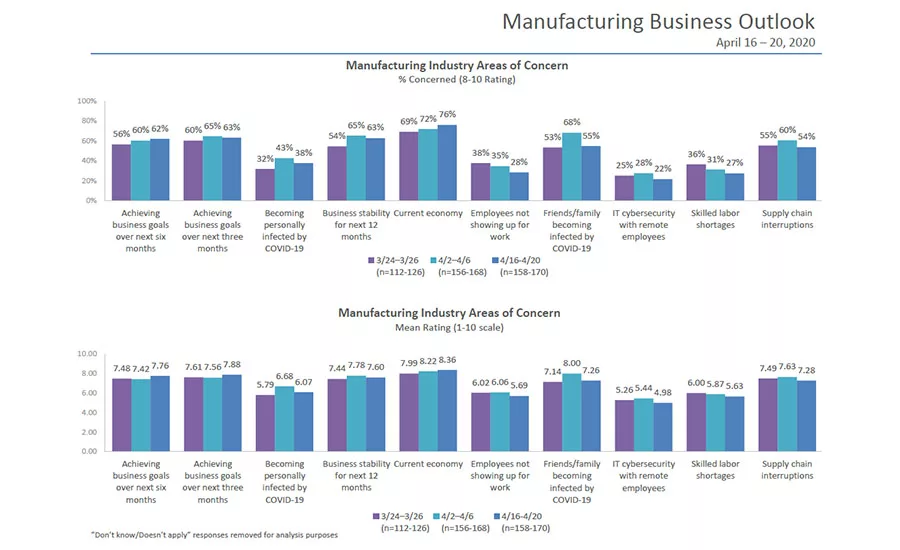

Consistent industry research allows HVAC contractors to track what is happening in the manufacturing sector of the economy. Research and image courtesy of Clear Seas Research.

As the COVID-19 pandemic surges through spring, HVAC manufacturing joins much of global industry in rolling back expectations for the remainder of 2020. Compared to a month ago, two areas of concern among manufacturers have noticeably dropped, according to a survey of manufacturers conducted April 16-20 by Clear Seas Research, the research arm of BNP Media (parent company to The ACHR NEWS). One of those decreased concerns is over friends, family, or employees becoming infected by COVID-19. The other is supply chain interruptions; 54 percent of manufacturers surveyed noted concerns in this regard, and while that’s still more than half, it’s down from 60 percent the first week of April.

“You get a little bit more wiggle room on this when the markets are declining, so even if we have some issues around production, we're able to absorb it in a natural way,” Todd Bluedorn, chairman and CEO of Lennox. “Even if we had 100 percent production capability, we would have to bring down our factories in any case to help manage the inventory levels.”

Looking further ahead, concern rose over achieving business goals over the next six months, up from 56 percent in late March to 62 percent in mid-April. Active business in mid-April has taken a blow, with 11 percent canceled, 33 percent delayed, and 56 percent still on schedule — as opposed to late March, when manufacturers reported 7 percent canceled, 26 percent delayed, and 67 percent still on schedule. Planned business sees 9 percent canceled, 41 percent delayed, and 50 percent on schedule, compared with just 6 percent canceled and 63 percent still on schedule a month ago.

Business spending (equipment, products, technology, service) shows a 75 percent decline since a year ago, and only 13 percent of manufacturers have noted an increase in new business development activity. Concerns about the current economy rose as well, up from 69 percent in late March to 76 percent in mid-April. And while 34 percent of manufacturers believe it will take three months or less for their business to get back on track, 37 percent believe it will take four to six months for this to happen.

Effects of COVID-19 on the Supply Chain

When states started issuing stay-at-home orders due to COVID-19, HVAC trade associations lobbied state and federal governments to make sure the industry was considered essential — from contractors to manufacturers. Francis Dietz, vice president of public affairs at AHRI, said he hasn’t had any supply-side issues in the U.S. For the last several weeks, the challenge has been Mexico.

“The Mexican government and the Mexican state governments obviously don't have guidance from the U.S. federal government,” he said. “Many of our members’ facilities down there are either are seriously impacted from the fact that several of the state governments have severely restricted some of our members operations. It’s been a really difficult situation, and it's ongoing.”

AHRI has been working with HARDI Mexico, trade representatives, and Mexican health inspectors and state government officials to break the stalemate, and appealing to the president of Mexico through the National Association of Manufacturers and the U.S. Chamber of Commerce.

Looking for quick answers on air conditioning, heating and refrigeration topics? Try Ask ACHR NEWS, our new smart AI search tool. Ask ACHR NEWS

“Sometimes we get a little glimmer of hope that things might get a little better, but we don't have anything concrete,” Dietz said.

Lennox’s residential factory productivity is expected to flip from a $10 million benefit to a $10 million headwind.

“Like most of industrial America, we're working our way through this,” said Bluedorn in a quarterly earnings call on April 20. “We have managed the supply chain well across regions that we source from, including Asia, and combined with our buffer stock, we've not seen an impact on our manufacturing factoring capability in this regard.

“In late March, we did make the decision to close some of our factories for a couple weeks…because we had some cases and also quite a few quarantines,” he said. These factories are now back up and running with protection for team members in place, albeit with varying levels of absenteeism as people stay away from work.

As far as the overseas supply chain, Asia is “now way in the rearview mirror,” with Mexico rising to the forefront, Bluedorn said. (As of a Feb. 27 update on operations in China, Emerson reported that 85 percent of its production employees have returned to work, and over 95 percent of its supply chain has restarted production; shipping time, however, had almost doubled and was costlier.)

Bluedorn noted that Lennox’s Mexican factories were never subject to government shutdown.

“We had the federal Mexican government come in and inspect us one afternoon, and we got a stamp of approval both as an essential industry, and also about all the processes that we were using to protect our people,” he said. “We took it down, just for production reasons, but we haven't taken it down because the government thought we should.”

Quarterly Results Due to the Pandemic

Lennox and Emerson announced quarterly financial results on April 20 and 21, respectively.

For 2020, Lennox expects a negative impact of 20 percent from COVID-19 on the North America unitary HVAC and refrigeration market. Bluedorn said forecasts were based on how HVAC markets performed during three prior downturns — the Asian financial crisis of the late 1990s, post-9/11, and the Great Recession.

“We have reset our financial expectations for the year based on that level of market impact and now expect revenue to be down 11-17 percent from last year, versus our previous guidance for growth of 4-8 percent,” he said.

“Looking at the various puts and takes in our financial assumptions for 2020, we now expect a benefit of $25 billion in net price for the year, compared to our previous guidance of $30 million,” said Lennox CFO Joseph Reitmeier. “For the industry overall, we now expect North American residential HVAC shipments to be down mid-teens, compared to prior expectations to be at mid-single digits, a 20-point negative impact from the COVID-19 pandemic. We expect both commercial unitary shipments and refrigeration shipments in North America to be down 25 percent, compared to our prior expectation for flat markets.”

Lennox repurchased $100 million of stock in the first quarter of 2020, has placed repurchase plans for the second quarter on hold, and will review plans for the third and fourth quarters as the year progresses; previous guidance was for $400 million of stock repurchases in 2020.

For Emerson, net sales of $4.2 billion were down 9 percent; underlying sales were down 7 percent, as demand declined significantly in March due to the rapid spread of COVID-19.

“The spread of the COVID-19 pandemic and associated uncertainty, social distancing, and business closure mandates negatively affected nearly all of our end markets and geographies, particularly in China, the United States, and Europe,” the company said in its financial statement. “One exception, however, was the surge in demand for products and solutions that support medical and life science end markets. Additionally, our businesses were negatively affected by the dramatic drop in oil and gas prices resulting from geopolitical tensions and a surge in global supply.”

Coronavirus and Construction Slowdown

Bluedorn said demand has slowed due to the pandemic from multiple sectors, and he anticipates it will continue to slow but at different rates.

“We saw contractors…stocking up less residential equipment ahead of the spring and summer seasons, due to the rising economic uncertainty, and national account customers in both our commercial and refrigeration businesses have pushed orders out,” he said. “I think the phenomena that you saw in first quarter will play out for a little bit longer, which is the starts that have started will continue, and so I wouldn't be surprised to see — in the near term — new construction up as add-on and replacement continues to go down. But I think certainly during the second half of the year, new construction will start to pull back significantly,” he said.

Demand business — where a contractor sees a job, buys the equipment, and installs it — is “actually hanging in there relatively well,” Bluedorn said. “It's down low single digits, but where we're seeing a real slowdown is dealers stocking up for the summer selling season; they're just not doing that, given all the uncertainty.”

New construction will continue until all the projects that have started wind down, he predicted.

“That hasn’t happened yet, but it will,” he said. “Planned replacement continues to flow for a little bit, until all the decision-makers decide what they need to do to pull back to get their companies lined up correctly.” Planned replacements have been slowing somewhat for the last two weeks, he reported.

“My experience … during 9/11 is, the marble rolls off the table on commercial quickly when it happens,” he said. “The marble hasn't rolled off yet — I mean, we’re down — but our guess is, it will.”

Emergency replacements, however, will continue to flow “even in tough times, because people need to buy HVAC,” Bluedorn predicted. “If we end up in a world, which it looks like we're going to, with 25-30 percent unemployment, people are going to try and band-aid their units. I think we'll see a spike up in repair parts and a decline in units.

“But just like we saw for the financial crisis, that demand doesn't go away; it just gets pushed out,” he continued. “And I'm looking forward to — I don't know if it's a year from now, or a year and a half from now — we'll have a new model out, and just like in ‘10, ‘11, and ‘12, we’ll have rising markets that are up double digits because all this pent-up demand will be unleashed. We're not Carnival Cruises. We're not Caesars Palace. It's not when this demand goes away, it never comes back, or you lose it forever. This demand gets pushed out. We're pushing it out, but it will come back.”

By the Numbers

Lennox

Negative impacts from the COVID-19 pandemic included lower volume and factory shutdown costs, higher other product costs, and unfavorable mix.

Revenue in the Residential Heating & Cooling business segment was $442 million, down 5 percent.

“Weather continued to have a significant adverse impact,” Bluedorn said. “Heating degree days were down from last year and every month, and down 15 percent overall for the quarter. Revenue from replacement businesses was down high single digits, impacted by the warm weather. New construction revenue was up high single digits, as the warm weather generally enabled homebuilders to get an early start in the year.”

Adjusted revenue in the Refrigeration business segment was $103 million, down 12 percent.

Revenue in the Commercial Heating & Cooling business segment was $178 million, up 3 percent. These results were impacted by favorable mix, lower material costs, and lower SG&A expenses.

"North America was down mid-single digits. Europe refrigeration and HVAC revenue was down high-teens as the impact from COVID-19 began to hit the already slower European market earlier than in North America,” Bluedorn noted.

Emerson

Automation Solutions net sales decreased 10 percent, with underlying sales down 8 percent. In the Americas, underlying sales were down 11 percent, with the United States down 12 percent, reflecting a broad-based drop in demand. Europe underlying sales were down 3 percent, while Asia, Middle East, and Africa underlying sales dropped 6 percent, driven by sharp declines in China of over 20 percent.

Commercial & Residential Solutions net sales decreased 7 percent with underlying sales down 5 percent. In the Americas, underlying sales were down 3 percent, reflecting a broad-based decline in demand as the quarter unfolded. Europe was down 1 percent as air conditioning market weakness more than offset demand in heat pump markets. Finally, Asia, Middle East, and Africa was down 15 percent, driven by a significant drop in China of over 30 percent.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!