Top 50 Distributors: Growth Continues

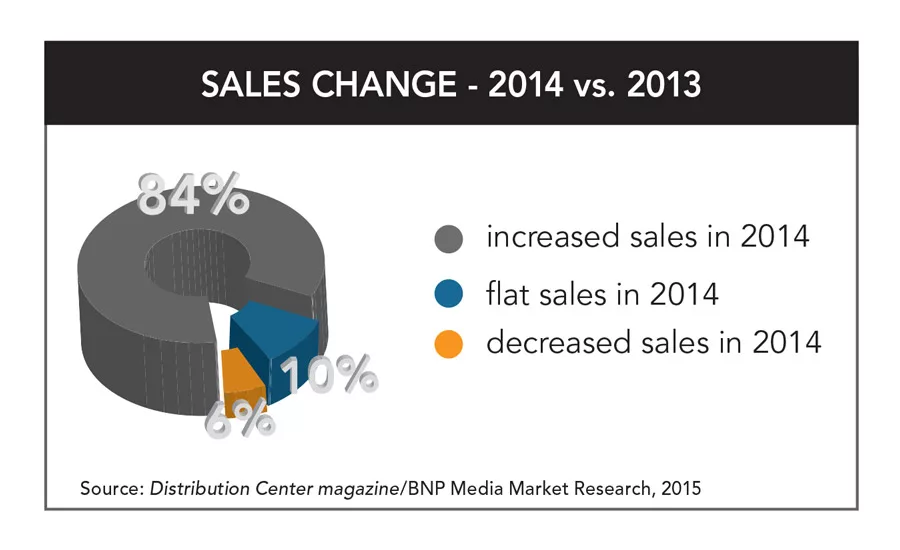

Last year, 91 percent of the Top 50 HVACR distributors projected increased sales for 2014, averaging growth of 9.1 percent. Those projections were not far off. This year’s survey found that 84 percent of the top 50 had a sales increase in fiscal 2014, averaging growth of 8.9 percent, and another 10 percent maintained flat sales year to year.

In November 2014, HARDI reported average sales for its distributor members had increased 9.4 percent, bringing the annualized growth through November to 6.9 percent.

“This year’s Top 50 reaffirms that it’s a good time to be in the HVACR industry, especially so if you’re an aggressive distributor willing to invest in growth-driving strategies,” said HARDI CEO Talbot Gee. “Looking at the 2015 list and the biggest movers, I see a consistent trend of investments in technology and service infrastructures that will position these companies to maintain and sustain consistent growth for the foreseeable future. I expect these companies to be aggressive in the acquisition market, especially the privately held firms, during this continued period of low interest rates. I am especially proud to see such an overwhelming representation of HARDI members in this year’s Top 50 as we continue to invest in advanced resources to help drive distributor growth.”

Affiliated Distributors members reported a 9 percent increase in same store sales of HVAC for 2014.

More than 80 distributors responded to this year’s Distribution Center magazine Top 50 HVACR Distributor survey, representing a total of $14.7 billion in HVACR sales. Among all respondents, 74 percent reported increased sales in 2014; 15 percent had flat sales, and 9 percent saw sales decrease.

The 2015 survey found that 19 of the 80+ respondents enjoyed double-digit HVACR sales growth in fiscal 2014. Conyers Winair Co., Conyers, Ga., a one-branch distributor that does not appear on the Top 50 list, reported a 24 percent increase in sales for 2014. Thos. Somerville Co., Upper Marlboro, Md., also not on the Top 50 list, said its 21 locations achieved a 19 percent sales increase for the company in 2014. Another distributor not in the Top 50, Mid-City Supply Co., Elkhart, Ind., which has six locations, reported an 18 percent sales increase for 2014.

Among the Top 50 ranked distributors, 14 indicated their HVACR sales had grown by 10 percent or more in 2014. The Granite Group, Concord, N.H., enjoyed a 21 percent rise in HVACR sales. Increases of 15 percent were reported by Williams, Distributing Co., Grand Rapids, Mich.; Lohmiller & Co., Denver, Colo.; Hercules Industries, Denver; Standard Supply & Distribution Co., Dallas; and Hajoca Corp. (estimated), Ardmore, Pa.

Looking for quick answers on air conditioning, heating and refrigeration topics? Try Ask ACHR NEWS, our new smart AI search tool. Ask ACHR NEWS

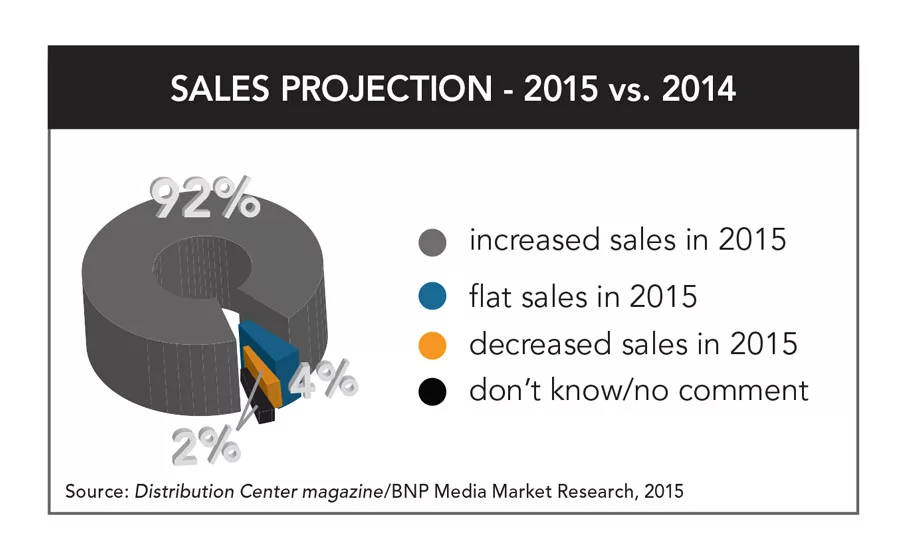

Projections for 2015 remain positive. Among all respondents to the survey, 88 percent said they expect HVACR sales to increase. Double-digit percentage increases were projected by 31 distributors. Also in the all-respondent group, 6 percent anticipate flat sales; 1 percent forecast a decrease and 4 percent said they don’t know.

Looking at just the Top 50 HVACR distributors, 92 percent said they expect sales to increase in 2015; 4 percent indicated sales will remain flat; 2 percent predicted a sales decline; and 2 percent had no comment or said they did not know. The highest percentage increase projected for 2015, 20 percent or more, was reported by two distributors in the Top 50: The Granite Group and Lohmiller & Co.

In the total group of respondents to this year’s survey, 91 percent said they were members of HARDI; among the Top 50, 96 percent said they were HARDI members.

A Closer Look at Performance

Watsco, Inc., Miami, Fla., remains at the top of the Top 50 list. The distributor enjoyed a 5 percent increase in HVACR sales in 2014. “Residential HVAC equipment sales in the U.S. jumped 8 percent with gains in market share, while commercial refrigeration products sale soared by 14 percent,” according to a report on Watsco by Zacks Investment Research.

The Zacks report said: “Watsco has been historically acquisitive, and its growth strategy focuses mainly on geographic expansion through market acquisitions, subsequently increasing revenues and profits from a combination of increased locations, products and services and improved management practices.”

HVAC represented 7 percent of ongoing 2013-2014 revenue for Newport News, Va.-based Ferguson Enterprises, according to its parent company Wolseley plc, in its annual report. “Branded dealerships of high quality equipment are an important feature of Ferguson’s HVAC market. Most revenue is generated by providing equipment and parts for the repair and replacement market,” Wolseley stated in the report. The HVAC business generated “good growth” in 2014, the company said.

Changes Among Distributors on the Top 50 List

Virginia Air Distributors, Midlothian, Va., was ranked No. 31 in last year’s Top 50, but this year is listed under the name of its parent company, Value Added Distributors, and ranked at No. 29. Value Added Distributors, or VAD, was formed in 2014 to serve as a parent company for what are three subsidiary companies. Virginia Air Distributors is the largest and most well-known; the other two are General Wholesale Distributors, GWD, in South Carolina, and Allied Heating and Cooling Sales Corp. in Virginia.

ACES A/C SUPPLY, Houston, was ranked No. 22 in last year’s Top 50. The families that operated ACES officially separated in September 2014, resulting in two companies: Shearer Supply, based in Carrollton, Texas, which is ranked No. 40 on this year’s Top 50 list; and ACES A/C Supply, based in Houston, which does not appear on this year’s list but we estimate would have been ranked No. 55. The company planned the separation years ago as new generations entered the business, and the two families – the Shearers and Davenports – remain friends and business partners, according to sources close to the company.

The biggest move up the list was by Hajoca Corp., ranked No. 13 in this year’s Top 50, up from No. 35 in last year’s survey. The company is ranked based on estimated figures. The distributor reportedly achieved a substantial increase in HVACR sales in 2014, plus sales of hydronic heating products were included in the estimate for the first time.

Standard Supply & Distributing Co., Dallas, jumped from No. 26 on last year’s Top 50 list to No. 20 on this year’s chart. The distributor also experienced a double-digit sales increase in 2014.

Certain other companies appearing on the 2015 chart also attributed higher sales to the inclusion of hydronic heating product sales in total HVACR sales reported for the first time this year.

For example, WinWholesale, Dayton, Ohio, moved up to No. 6 from No. 10 on the Top 50 chart, based on a substantially larger HVACR sales figure for 2014 that the company was able to determine with an improved financial reporting tool, combined with the inclusion of hydronic heating sales that were not so easily identifiable in past years and thus not included.

Two companies are new to this year’s top 50 ranking: Goodin Co., Minneapolis, Minn., ranked at No. 47, and Williams Distributing Co., Grand Rapids, Mich., ranked No. 50. Two companies that appeared on last year’s Top 50 are not on this year’s: Meier Supply Co., Conklin, N.Y., No. 49 last year, was at No. 52 this year; and McCall’s Inc., Johnsonville, S.C., ranked No. 44 last year, was at No. 53 this year.

In April 2015, private equity investment firm Rotunda Capital Partners announced it had acquired a majority stake in Munch’s Supply Co. Inc., ranked No. 28 in this year’s Top 50 list. They did not disclose financial terms.

Based in New Lenox, Ill., Munch’s operates seven branches in Chicago and Northwest Indiana. CEO Robert Munch and his management team will continue to lead the company, Rotunda Capital said in a statement.

“The firm brings tremendous expertise in the distribution space, and we’ve outlined a strategy together that will allow us to aggressively expand to new regions while continuing to invest in our core Chicago market,” Robert Munch said in a statement.

Sales Breakdowns

Of the distributors on the 2015 Top 50 list, 41 said 50 percent or more of their total company sales was generated by HVACR; of these, 35 distributors reported 90 percent or more of their total company sales was in HVACR.

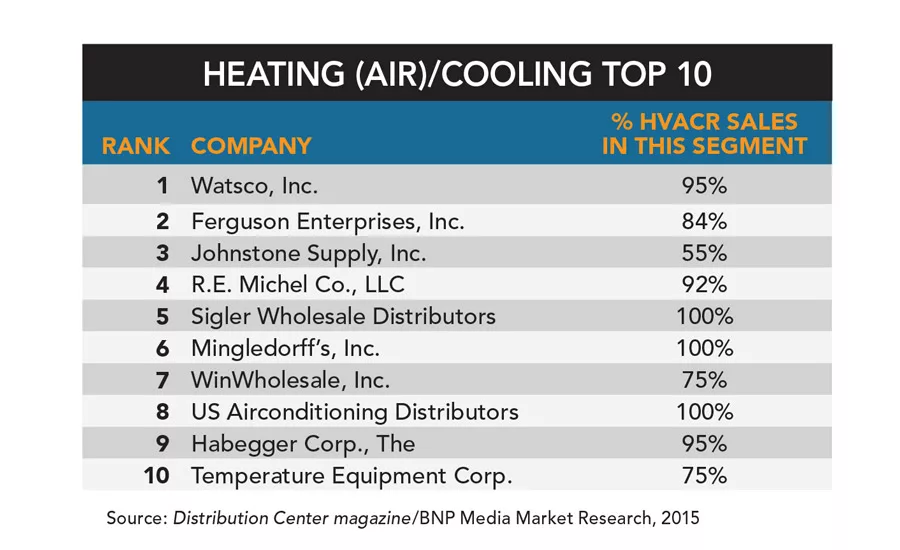

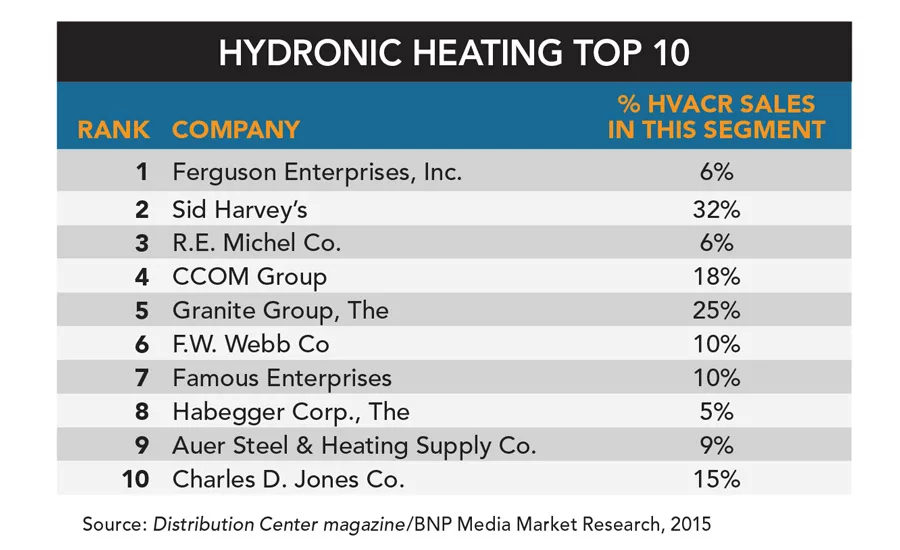

The breakdown of HVACR sales by category was: 83 percent heating (air)/cooling; 5 percent hydronic heating; 7 percent refrigeration; and 5 percent other. The “other” HVACR category included items such as: heating/cooling controls; pipe, sheet metal; variable refrigerant flow (VRF); plumbing, PVF; accessories; parts; tools; supplies, materials; solar; ground source.

Factors Expected to Impact HVACR Distribution in 2015

Distributors were asked to identify which specific factors would most impact HVACR distribution in 2015.

• “The general economy in some of our markets,” said Lanny Sigler, vice president, Sigler Wholesale Distributors, Tolleson, Ariz., ranked No. 5 both this year and last year.

• “The weather,” said Jeff New, president, Mid-City Supply Co., Elkhart, Ind.

• “Regional standards have complicated inventory management, especially for distributors that are right on border states,” said Brad Muehlbauer, president, Koch Air, LLC, Evansville, Ind., ranked No. 16 this year.

• “Movement toward higher efficiency heating and cooling systems in both residential and commercial areas,” said Gene Boos, senior vice president, S.W. Anderson Sales Corp., Farmingdale, N.Y.

Other responses regarding factors affecting the industry from distributors who asked not to be named included:

Labor, employment numbers, oil prices, talent shortage, SEER ratings, refrigerant legislation, energy prices, R-22 allocations, product availability, climate, supplier production, residential new construction, weak macro economic factors, weak new construction cycle, large contractor market share increases, change in Congress, reduced government interference, variable refrigerant flow, price competition, utility rebates, mini-split technology, home remodeling, interest rates, housing, technology, mix change due to 14 SEER mandate, increase in selling complete systems and commercial ductless splits.

General Observations on the HVACR Industry

“I remain very concerned about many policies coming out of Washington that too often actually discourage economic growth, and sometimes are openly hostile to business,” commented Lanny Sigler of Sigler Wholesale Distributors. “Too often, our politicians want to punish success, and that attitude has grown throughout our society.”

Gene Boos of S.W. Anderson Sales noted, “Though competition maintains a level of price sensitivity, there is a building trend toward value-added services.”

Observations made by other distributors, who asked not to be named, included:

• “E-Commerce threats, such as Amazon Supply & Grainger.”

• “We expect the Texas market to be negatively affected by declining oil prices. The large inventory of 13 SEER equipment will be positive.”

• “Fluctuations in the price of R-22 have caused wild swings in HVACR sales. The change in refrigerants and the weather have impacted business, and we expect that impact to continue.”

In a piece posted on the Distribution Center magazine website, Geoff Godwin, vice president, marketing, Emerson Climate Technologies, White-Rogers, discussed the challenges faced by HVACR distributors in 2015. Here are a few excerpts:

“One of the top challenges for 2015 will be keeping up with the changing regulatory environment, including regional standards for residential unitary air conditioning and heat pump systems and part-load efficiency requirements for light commercial split, package and rooftop systems and 2015 chiller standards.

“On the residential side, there is still confusion about enforcement of the regional efficiency standards, and this issue is especially challenging for wholesalers on regional border states.

“When it comes to the growing interest in applying HVAC to the connected home, those of us in the industry need to assert our leadership.”

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!