HARDI Distributors Report 'Sales Thud' of 8.7%

COLUMBUS, Ohio — The latest report from Heating, Air-conditioning & Refrigeration Distributors International (HARDI) showed that sales among distributors participating in HARDI’s monthly sales survey fell by 8.7% in March.

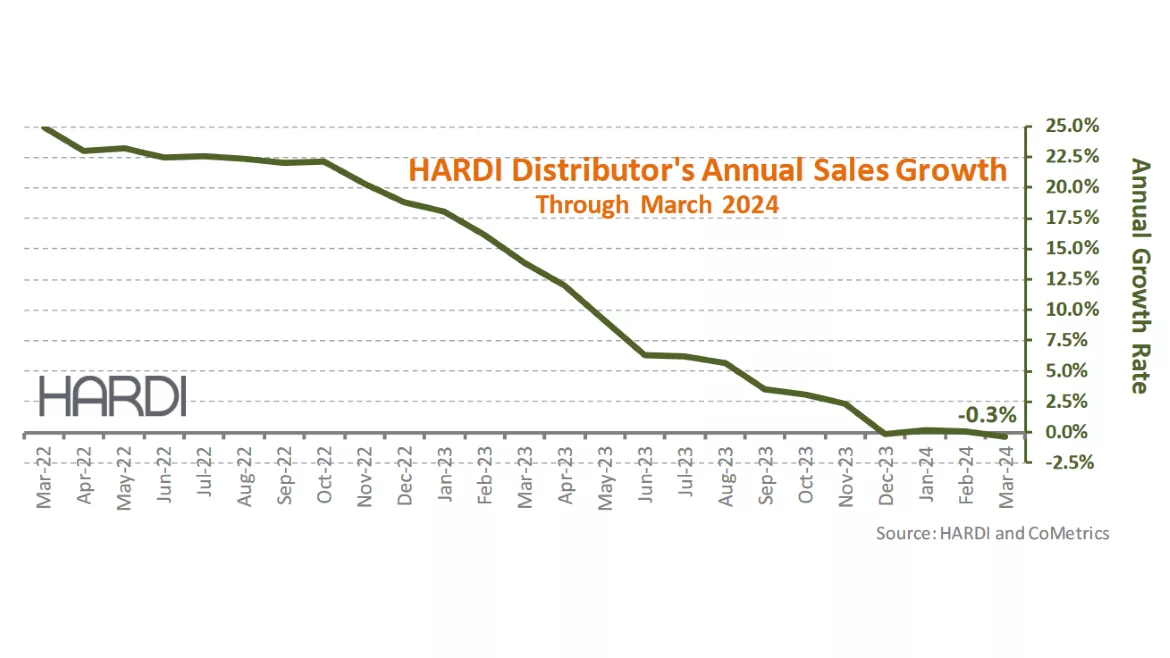

Annual sales for the 12 months through March 2024 declined by 0.3%.

“There were two important factors behind the sales thud at the end of heating season,” said Brian Loftus, HARDI’s macroeconomic and residential market analyst, in a press release. “Heating degree days during March of 2024 were off by 16% from the prior year, which may have trimmed sales year-to-year, but the main reason for the decline is March of 2023 had two more billing days. We estimate sales were about flat with the same number of billing days.”

The Days Sales Outstanding, a measure of how quickly customers pay their bills, was near 41 days during March, as it was during March 2023. “Forty-one this month was comparable to March of 2022 and better than March of 2021 and 2022,” said Loftus. “There have been a lot of market headwinds during the past 12 to 18 months, but not enough to compromise dealer’s bill-paying ability.

“The annual sales growth has been flat during the past four months, but we expect that to improve,” Loftus continued. “The number of home listings is finally starting to improve, and the pace of existing home sales has steadied. Single-unit permits are increasing, and the Fed’s next move will be a rate cut. It looks like the cycle is turning.”

HARDI members do not receive financial compensation in exchange for their monthly sales data and can discontinue participation without prior notice or penalty. Participation is voluntary, and the depth of market coverage varies from region to region. An independent entity collects and compiles the data, which can include sales information about products not directly associated with the HVACR industry.

Looking for quick answers on air conditioning, heating and refrigeration topics? Try Ask ACHR NEWS, our new smart AI search tool. Ask ACHR NEWS

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!