Double-Digit Growth Dominates Top 50 List, Watsco Inc. Ranked First

Many HVACR Distributors Celebrating a Good Year

It’s been a good year; even better than expected. That’s the data and the sentiment coming from Distribution Center’s 2014 Top 50 HVACR Distributors.

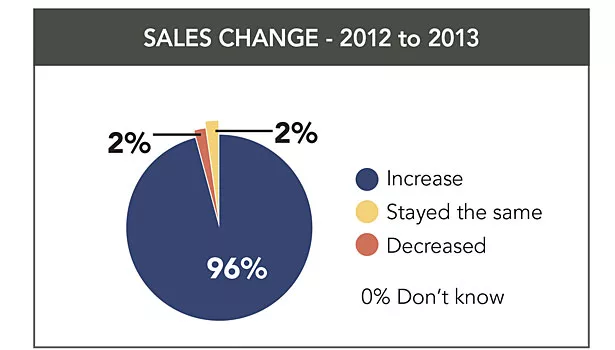

Last year’s Top 50 survey found that 84 percent of respondents expected their sales to increase in 2013. The year turned out even stronger than projected, with 96 percent of this year’s respondents reporting increased sales in fiscal 2013. Of the top 50 distributors, 22 companies experienced double-digit percentage sales increases.

Click Here to View the List of the 2014 Top 50

Download a Print-Friendly PDF Version of the List

In the first Top 50 HVACR Distributors study published in May 2012, the top 50 companies represented more than $10.3 billion in HVACR sales for fiscal 2011. Last year, the Top 50 HVACR Distributors generated more than $11.5 billion in HVACR sales for fiscal 2012. This year’s study revealed that the Top 50 HVACR Distributors accounted for $12.8 billion in HVACR sales for fiscal 2013.

Comparing the Top 50 Distributors listed in 2013 with this year’s list, some new faces have appeared: Jackson Supply, Houston; S.W. Anderson Sales Corp., M&A Supply Co., AC Pro, The Granite Group, Robertson Heating Supply, and Meier Supply Co.

Along with new faces and increased sales, the survey asked distributors to specify what percentage of their HVACR sales was represented by each of the following segments, adding up to 100 percent: HVAC heating air side/cooling equipment and supplies; hydronic heating; refrigeration; and other.

Sales for the Top 50 Distributors broken down by segment are as follows: 81 percent HVAC, 3 percent hydronic heating, 8 percent refrigeration, and 9 percent were other. See charts for details.

Looking for quick answers on air conditioning, heating and refrigeration topics? Try Ask ACHR NEWS, our new smart AI search tool. Ask ACHR NEWS

Respondents identified “other HVACR” as including other commodities such as pipe and sheet metal; controls; machinery; parts; tools; plumbing; equipment; geothermal; duct, insulation; testing equipment; indoor air quality; and pipe fittings.

Confirming Predictions

Looking back to 2011, Alan Beaulieu, senior economist for ITR, told attendees at the HARDI Annual Conference in Hawaii that they would be busier and likely to make more money in 2012 and should expect to be even busier in 2013.

The first annual Top 50 HVACR Distributors report, published in May 2012, revealed that 80 percent of respondents saw increased HVACR sales in fiscal 2011 versus 2010, and 79 percent said they expected 2012 HVACR sales to surpass 2011.

The 2013 report, based on fiscal 2012 HVACR sales, found that 17 of the top 50 distributors experienced a 10 percent or higher boost in their HVACR sales, and six of those reported increases were 15 percent or more. Among all of the companies that responded (more than 90), 73 percent said their HVACR sales had increased in 2012.

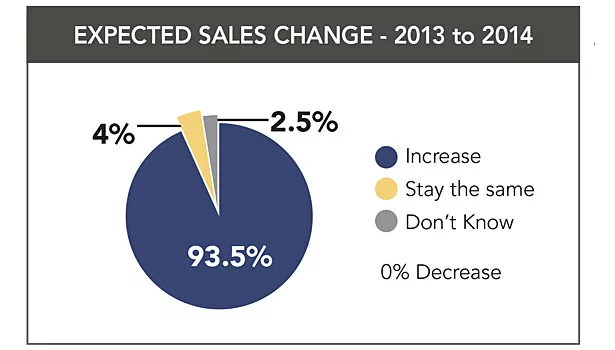

The positive outlook continues to prevail, with 91 percent of this year’s survey respondents projecting sales increases for fiscal 2014. The average increase predicted is 9 percent. No one projected a sales decrease for 2014; those respondents who did not project an increase answered with “stay the same” or “I don’t know.”

“It’s great to see significant growth return to our channel, and even better to see how generally widespread it is,” said Talbot Gee, executive vice president and COO, HARDI. “While acquisitions have started to pick up again, it’s important to note how diverse the HVACR distribution channel continues to be with only four of the top 50 distributors having more than $500 million in annual HVACR sales. This demonstrates the growth potential that lies in being a dominant local and regional player despite the success and growth of the multi-regional and national distributors. I view this as a sign of strength and health in our channel, and another reason for confidence in independent HVACR wholesale distribution going forward.”

Of the more than 80 companies that responded to the survey, only nine were not members of HARDI. Among the top 50, 94 percent are HARDI members.

Analyzing 2013 Sales

Sigler Wholesale Distributors, Tolleson, Ariz., was one of the Top 50 to report a double-digit percentage sales increase in 2013.

“The 14 percent sales increase in 2013 does not represent sizable growth in the overall economy but can be attributed to our company getting more of the available business in some of the newer markets we are serving, such as California,” said Lanny Sigler, vice president, Sigler Wholesale Distributors.

Famous Enterprises, Akron, Ohio, which took a big leap up in the ranking chart this year due to a substantial sales increase in 2013, cited internal growth as the primary driving factor. Sources close to the company attributed the increase to two new branches — one small, one medium — that opened last year and a powerhouse team that has added new customers and helped to grow business with existing customers.

Five companies that responded to the survey, four of which made the top 50 list, had sales increases of 20 percent or higher in 2013 compared with 2012. These achieving companies are: Mingledorff’s, Norcross, Ga.; Famous Enterprises, Akron, Ohio; AC Pro, Fontana, Calif.; Robertson Heating Supply, Alliance, Ohio; and American Air Distributing, West Chester, Pa.

Another dozen distributors reported increases of 15 to 19 percent when comparing 2013 to 2012: US Airconditioning Distributors, City of Industry, Calif.; F.W. Webb Co., Bedford, Mass.; Morrison Supply Co., Fort Worth, Texas; Slakey Brothers, Sacramento, Calif.; Jackson Supply Co., Houston; Standard Supply; M&A Supply Co., Brentwood, Tenn.; The Granite Group, Concord, N.H.; United Supply, North Plainfield, N.J.; Robinson Supply, Fall River, Mass.; Aaron and Co., Piscataway, N.J.; and Wolff Bros. Supply, Medina, Ohio.

Ten other distributors enjoyed sales increases of 10 to 14 percent in 2013, including R.E. Michel Co., Glen Burnie, Md.; Sigler Wholesale Distributors, Tolleson, Ariz.; Gustave A. Larson Co., Pewaukee, Wis.; Auer Steel & Heating Supply, Milwaukee; Munch’s Supply, New Lenox, Ill.; Hercules Industries, Denver; Hajoca Corp., Ardmore, Pa. (estimated); Lohmiller & Co., Denver; S.W. Anderson Sales, Farmingdale, N.Y.; and McCall’s, Johnsonville, S.C.

“The Waterworks and HVAC businesses grew strongly,” Wolseley plc, the Switzerland-based parent company to Ferguson, said in its annual report. “Revenue in the USA was 8.2 percent ahead of last year on a like-for-like basis including price inflation of approximately 1 percent. HVAC accounted for 7 percent of revenue for the U.S. operations.”

Revenues for Watsco, Coconut Grove, Fla., increased 9 percent in fiscal 2013; same-store sales improved 7 percent reflecting a 9 percent increase in HVAC equipment sales, and 3 percent sales increase in both other HVAC products and commercial refrigeration products, according to coverage of the company’s earnings performance by Zacks Equity Research. Watsco’s residential HVAC equipment sales rose 17 percent and other HVAC product sales were up 8 percent, Zacks reported. According to Watsco, the company’s growth was aided by higher sales, stronger selling margins, and continued operating cost management.

In-depth Outlook

Among the distributors who reported double-digit sales increases in 2013, 21 projected a somewhat lower percentage sales increase in 2014. In many cases, the difference was only a few percentage points less.

“Based on our formal budgeting process for the year, which is based on what we learn from looking at all of our markets and territories individually and talking to managers and people in the field, I am reducing the sales growth projection for 2014 to 7 percent,” said Sigler. “This also is based on the first three months of 2014. The economy is definitely improving, but it is not growing very fast. In general, we are still really excited and optimistic about our Southwestern markets, but it is somewhat disappointing that the economy has been so tepid. It is not where it could or should be. We are pleased with our performance, but it could be much better if the economy was better.”

Watsco has “immense potential” in the replacement market due to the aging stock of air conditioners and heating systems in the United States, according to a published report by Zacks Equity Research.

“Watsco’s joint venture with Carrier Corp., a wholly owned subsidiary of United Technologies Corp., continues to generate profits. The company intends to purchase an additional 10 percent interest in the venture in the Sun Belt region in 2014.”

Without the tax incentives on HVAC products other than geothermal, there could be a slight drop in top efficiency products this year, noted Brett E. Mattison, president, Decker & Mattison Co. Inc., dba/Freeman Supply Co. Inc., Hutchinson, Kan.

“Geothermal sales should increase this year with the available tax incentives through 2016 and along with the higher utility prices we are currently seeing throughout the United States,” he commented.

Increased building tightness and efficiency will make it mandatory for ventilation of fresh air, noted Kurt Johnson, owner, Fresh Air Ventilation Systems, Lewiston, Maine.

“Studies showing moisture and pollution increases inside will increase the push for regulations to be stepped up. With the high cost of health care in this country, we can’t afford to allow indoor air pollution because of energy efficiency concerns to overshadow the health damage being done to the occupants of our buildings. Energy efficiency becomes secondary to people’s health. Right now, that is not being prioritized as it should be. The United States lags behind on this issue.”

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!