R-22 Uncertainty Keeps Distributors on Edge

Industry Pushes for Aggressive Timeline as EPA Develops Final Rule

HARDI is pushing for an aggressive linear approach as the EPA develops the final rule for the phaseout of hydrochlorofluorocarbon (HCFC) refrigerants by 2020.

As the U.S. Environmental Protection Agency (EPA) wraps up the comment period for its final hydrochlorofluorocarbon (HCFC)-22 allocation rule for 2015-2019, the industry leaders who have been pushing for a more aggressive approach to the phaseout are now left to wait and see what the EPA does.

But, due to the time and steps it takes to develop the rule, the EPA may not release its Final Rule until the end of the year. That delay is causing great uncertainty for many distributors and wholesalers, said Jon Melchi, director of government affairs at HARDI.

“We believe it’s imperative that the allocation rule come out as fast as possible,” Melchi said. “Distributors need time to plan their business strategies for 2015, and it’s challenging to forecast when you are unsure what the allocation will be.”

WEIGHING THE OPTIONS

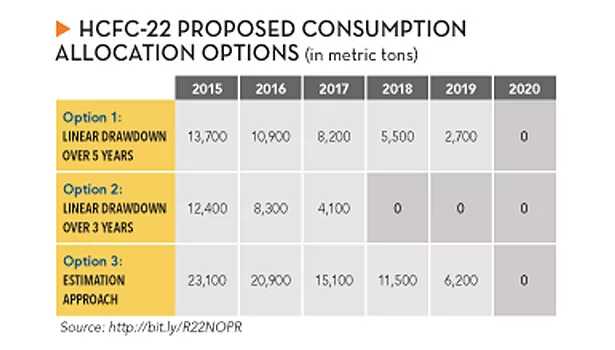

While HARDI has advocated for an aggressive linear approach to the phasedown, the EPA has also taken comments from groups that advocate for zero allocation in 2015, including refrigerant reclaimers and environmental organizations — a position HARDI has disagreed with. Meanwhile, the EPA has outlined three potential schedules leading up to the eventual phaseout of R-22 by 2020.

In its Notice of Proposed Rulemaking published in the Federal Register on Dec. 24, 2013, the EPA outlined those options:

• Option 1: Linear Drawdown Over 5 Years. R-22 production is 13,700 metric tons (30 million pounds) in 2015; 10,900 metric tons (24 million pounds) in 2016; 8,200 metric tons (18 million pounds) in 2017; 5,500 metric tons (12 million pounds) in 2018; 2,700 metric tons (6 million pounds) in 2019, and zero in 2020.

• Option 2: Linear Drawdown Over 3 Years. R-22 production is 12,400 metric tons (27 million pounds) in 2015; 8,300 metric tons (18 million pounds) in 2016; 4,100 metric tons (9 million pounds) in 2017, and zero in 2018 and beyond.

• Option 3: Estimation Approach. R-22 production is 23,100 metric tons (51 million pounds) in 2015; 20,900 metric tons (46 million pounds) in 2016; 15,100 metric tons (33 million pounds) in 2017; 11,500 metric tons (25 million pounds) in 2018; 6,200 metric tons (13 million pounds) in 2019, and zero in 2020.

Looking for quick answers on air conditioning, heating and refrigeration topics? Try Ask ACHR NEWS, our new smart AI search tool. Ask ACHR NEWS

Option 1 is the EPA’s preferred approach to the R-22 phaseout, and Melchi said he has yet to hear “from a single person in this industry — whether a producer, distributor, contractor, or reclaimer — who thinks that the allocation should be more than the EPA’s preferred approach.”

Melchi added that a linear drawdown schedule would help provide some certainty for their members while also stabilizing R-22 prices.

“What we’ve seen is that drastically cutting and adding supply into the marketplace has a significant financial impact on our members,” he said. “That needs to be explained to people.”

BAD BUSINESS

In addition to the R-22 that may be produced over the next few years, there is still a supply of R-22 in the marketplace following the EPA’s decision to increase the amount produced from 55 million pounds in 2012 to 62.8 million pounds in 2013. The resulting surplus of R-22 caused prices to plummet, hurting the reclamation and retrofit markets as consumers chose to stick with R-22 instead of retrofitting their equipment to use non-HCFC refrigerants.

FIVE ISSUES TO WATCH IN 2014 OrganizationWhile legislation is passed and regulations developed each year that affect small businesses, a few stand out above the rest as issues that could significantly impact distributors, in particular. Jon Melchi, director of government affairs HARDI, points out five such issues: 1 The ongoing regional standards lawsuit. “If the case goes the distance, it could last until the end of the year. There’s always hope for a settlement agreement, but absent that, I think you will see a motion to try and stay the [Jan. 1, 2015] implementation date for air conditioner regional standards,” Melchi said. 2 Implementation of the Affordable Care Act. “No other issue is going to have as big an impact across all of our members,” Melchi said. 3 Online sales tax. “I think we’re going to see a little more action on the Marketplace Fairness Act, which deals with the tax on online sales,” Melchi said. “There will probably be a renewed push on that coming soon.” 4 Reforming the tax code. “Some studies show that for distributors and retailers, the effect of tax rates on them is significantly higher than other lines of trade, and we don’t necessarily think that’s fairness in the tax code,” Melchi said. “Having said that, many folks think tax reform is a ticket to repeal LIFO, and we oppose that wholeheartedly.” 5 Other regulatory actions from the U.S. Department of Labor (DOL), Occupational Health and Safety Administration (OSHA), the National Labor Relations Board (NLRB), U.S. Department of Energy, etc. “They may have significant effects on the operation of our members’ businesses,” Melchi said. |

Troy Meachum, president at ACR Supply Co., Durham, N.C., said the unpredictable supply of R-22 has negatively affected many companies, including his.

“We lost money,” he said. “The R-22 market, for most suppliers, has become a profit loss and a source of great confusion. We buy based on the economics we see at the time of purchase with expected due diligence, then the market and external pressures quickly places this product at a loss.”

Bill Bergamini, president, ILLCO Inc., Countryside, Ill., said the industry had been gaining momentum in transitioning away from the ozone-depleting refrigerant a year ago, but when production was increased in 2013, “more supply than was anticipated was put back into the market.” With lower prices and more supply than demand, “the end goal of transitioning away from R-22 has lost all momentum,” he said.

“We are six short years from a total phaseout of R-22 and are going in the wrong direction,” Bergamini added.

GETTING BACK ON TRACK

While the R-22 surplus has negatively affected the industry, Melchi warns that bringing production down to zero in 2015 would also cause the industry great hardship.

“We’re not going to argue that there’s an oversupply,” Melchi said. “There was certainly more allocated in 2013 and 2014 than we would’ve hoped. But what we also caution against is assuming that because X pounds of R-22 have been stockpiled, the same amount would be for sale next year if the zero approach were to be taken. There are a lot of variables.”

Taking the linear drawdown approach will “make things much easier on the industry, including manufacturers that have to kind of forecast the market,” Melchi explained. “If they’re making compressors and then you cut it off, it throws the whole thing up in the air. What we need to do is figure out a responsible way to get this down to zero in 2020, and I don’t know that the zero approach is the most responsible way for us to get there.”

Meachum agreed that an aggressive linear drawdown is the best approach for the industry.

HARDIPAC FORMEDIn 2013, HARDI announced the formation of HARDIPAC, a political action committee (PAC). HARDIPAC has been established to support federal candidates who understand small business and promote policies which will help our industry grow. HARDIPAC was established by a vote of the HARDI board of directors and will be governed by a committee of seven HARDI distributors. The committee consists of: Bud Mingledorff — Mingledorff’s Inc., President Karen Madonia — Illco Inc., Treasurer Matt McGarry — ABR Wholesalers Inc. Greg Grimme — Johnstone Supply Dan Hinchman — Aireco Supply Inc Richard Cook — Johnson Supply Russ Geary — Geary Pacific Supply “HARDIPAC is a sign of strength and unity for our industry,” said Madonia, HARDIPAC treasurer. “Every day distributors across the county are impacted by policy decisions from Washington, whether they have to do with the estate tax, threats to LIFO, changes to our health care system or a never-ceasing regulatory system. HARDIPAC will allow us to join together and promote the issues that are important to the HVACR distribution community to the people who are making these decisions.” To learn more about HARDIPAC, email Jon Melchi at jmelchi@hardinet.org. |

“As the available R-22 remains high and the demand low, the movement toward reclaim and retrofit gases will also follow a linear path and can expect to be slower, too,” Meachum explained. “The stated opinion of HARDI to the OMB [Office of Management and Budget] and the EPA is that a linear phasedown at a faster rate would stabilize the market faster, raise the reclaim [amounts] faster, and move to the alternative [refrigerants] faster — all three things the EPA states they would like to see, and all three things distribution would like to see too.”

Bergamini also agreed that an aggressive drawdown has always been the best option. “My position has not changed in regards to the supply of R-22 in the market,” he said. “I think the EPA needs to cut production as deep as possible, as soon as possible.”

THE WAITING GAME

Following the comment period, the EPA begins work on the final rule, which could take months to complete.

“They’ll have to take all the comments, then they’ll have to write the rule, and then it gets kicked to the OMB,” Melchi said. “This is likely not going to be finalized until the fourth quarter of this year.”

Meachum said he is concerned about “not knowing the final rule and how it might change.”

Melchi said they have done what they can to try to educate and influence the EPA throughout the rulemaking process.

“We’ve said in multiple public comments that the phasedown should be aggressive, and that they should get it done quickly and with a result that can be explained easily throughout the supply chain and to the end user,” Melchi said. “We’ve just been consistent in that we want it to be a swift phasedown, have the rule done quickly, have it be easily understandable, and have this transition be as transparent and as easy as possible so people can get on with their business.”

To read the EPA’s Notice of Proposed Rulemaking, visit http://bit.ly/R22NOPR.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!