An Update to the Budget and Economic Outlook 2016 to 2026

The deficit under current law is projected to be larger this year, but smaller over the 2017 – 2026 period, than CBO projected in March. Since January, CBO has reduced its projections of GDP growth and interest rates over the coming decade.

In fiscal year 2016, the federal budget deficit will increase in relation to economic output for the first time since 2009, CBO estimates. If current laws generally remained unchanged — an assumption underlying CBO’s baseline projections — deficits would continue to mount over the next 10 years, and debt held by the public would rise from its already high level.

CBO’s estimate of the deficit for 2016 has increased since the agency issued its previous estimates in March, primarily because revenues are now expected to be lower than earlier anticipated. In contrast, the cumulative deficit through 2026 is smaller in CBO’s current baseline projections than the shortfall projected in March, chiefly because the agency now projects lower interest rates and thus lower outlays for interest payments on federal debt. Nevertheless, by 2026, the deficit is projected to be considerably larger relative to gross domestic product (GDP) than its average over the past 50 years.

CBO’s economic forecast — which serves as the basis for its budget projections — indicates that, after a tepid expansion in the first half of 2016, economic growth will pick up in the second half of the year. That faster pace is expected to continue through 2017 before moderating in 2018. In CBO’s estimation, the faster growth over the next two years will spur hiring, increase employment and wages, and put upward pressure on inflation and interest rates. In the latter part of the 10-year projection period, however, output will be constrained by a relatively slow increase in the nation’s supply of labor.

The growth in GDP that CBO now projects is slower throughout the 2016–2026 period than the agency projected in January. Weaker-than-expected economic growth indicated by data released since January, recent developments in the global economy, and a reexamination of projected productivity growth contributed to that downward revision. The reduction to CBO’s projections of interest rates reflects the revisions to projected economic growth as well as CBO’s reassessment of the future demand for Treasury securities.

The Budget Deficit for 2016 Will Be About One-Third Larger Than Last Year’s

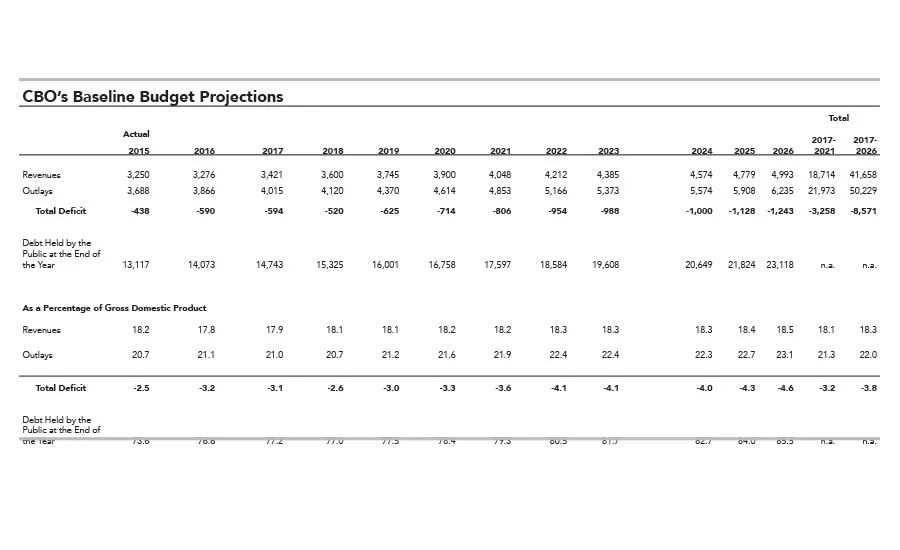

CBO now estimates that the 2016 deficit will total $590 billion, or 3.2 percent of GDP, exceeding last year’s deficit by $152 billion (see table below). About $41 billion of that increase results from a shift in the timing of some payments that the government would ordinarily have made in fiscal year 2017; those payments will instead be made in fiscal year 2016 because October 1, 2016 (the first day of fiscal year 2017), falls on a weekend. If not for that shift, the projected deficit in 2016 would be $549 billion, or 3.0 percent of GDP — still considerably higher than the deficit recorded for 2015, which was 2.5 percent of GDP.

Looking for quick answers on air conditioning, heating and refrigeration topics? Try Ask ACHR NEWS, our new smart AI search tool. Ask ACHR NEWS

The deficit is growing in 2016 because revenues are up only slightly, by less than 1 percent ($26 billion), whereas outlays are projected to rise by 5 percent ($178 billion). As a share of GDP, total revenues are expected to fall from 18.2 percent to 17.8 percent. In contrast, outlays are projected to rise to 21.1 percent of GDP, up from 20.7 percent last year. That increase is the result of the following: a 6 percent rise, in nominal terms, in mandatory spending for programs such as Social Security and Medicare (which is generally governed by statutory criteria); a 1 percent increase in discretionary outlays (which stem from annual appropriations); and an 11 percent jump in net interest outlays. Debt held by the public will amount to nearly 77 percent of GDP by the end of 2016, CBO estimates — 3 percentage points higher than last year and its highest ratio since 1950.

Growing Deficits Projected Through 2026 Would Drive Up Debt

In CBO’s baseline projections, the budget deficit is generally on an upward trend over the next decade, reaching 4.6 percent of GDP in 2026. A slight decline in the deficit over the next two years is largely explained by the shift in the timing of payments from one fiscal year to another because certain scheduled payments fall on weekends. In later years, continued growth in spending — particularly for Social Security, Medicare, and net interest — would outstrip growth in revenues, resulting in larger deficits and increasing debt.

Outlays

In CBO’s projections, annual federal outlays rise by $2.4 trillion (or about 60 percent) from 2016 to 2026. Relative to the size of the economy, outlays remain near 21 percent of GDP for the next few years — higher than their average of 20.2 percent over the past 50 years. Later in the coming decade, the growth in outlays would exceed growth in the economy, and by 2026, outlays would rise to 23.1 percent of GDP. That increase reflects significant growth in mandatory spending and interest payments, offset somewhat by a decline, in relation to the size of the economy, in discretionary spending. More specifically:

Outlays for mandatory programs are projected to rise by close to 70 percent in nominal terms from 2016 to 2026, increasing as a percentage of GDP by almost 2 percentage points over that period. That increase is mainly attributable to the aging of the population and rising health care costs per person, which substantially boost projected spending for Social Security and Medicare.

Because of rising interest rates and, to a lesser extent, growing federal debt, the government’s interest payments on that debt are projected to rise sharply over the next 10 years —nearly tripling in nominal terms and almost doubling relative to GDP.

In contrast, discretionary spending is projected to rise by a much smaller amount in nominal terms, consequently dropping to a smaller percentage of GDP than in any year since 1962 (the first year for which comparable data are available).

Revenues

If current laws generally remained unchanged, revenues would gradually rise — by $1.7 trillion, or about 50 percent, from 2016 to 2026 — increasing from 17.8 percent of GDP in 2016 to 18.5 percent by 2026. They have averaged 17.4 percent of GDP over the past 50 years.

Only revenues from individual income taxes would grow faster than the economy. In CBO’s baseline, with revenues from each source measured as a percentage of GDP:

Receipts from individual income taxes increase each year—for a total rise of 1.3 percentage points over the 10-year period—because of real bracket creep (the process in which, as income rises faster than prices, an ever-larger proportion of income becomes subject to higher tax rates), rising distributions from tax-deferred retirement accounts, an increase in the share of wages and salaries earned by higher-income taxpayers, and other factors.

Remittances from the Federal Reserve, which have been unusually high since 2010, return to more typical levels, dropping by 0.4 percentage points from 2016 to 2026.

Payroll tax receipts decline by 0.2 percentage points over the next decade, primarily because of the expected increase in the share of wages going to higher-income taxpayers.

Corporate income tax receipts change little over the 10-year period.

Debt Held by the Public

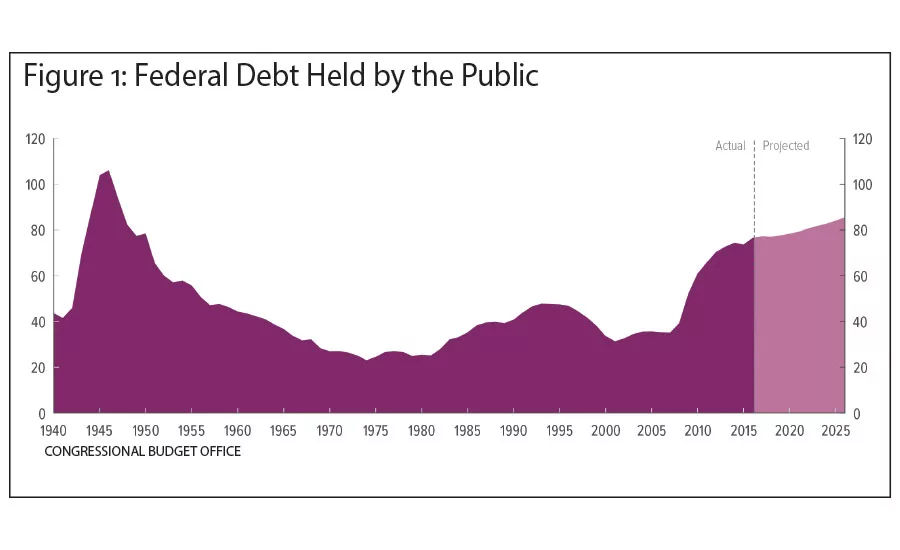

As deficits accumulate in CBO’s baseline, debt held by the public rises from 77 percent of GDP ($14 trillion) at the end of 2016 to 86 percent of GDP ($23 trillion) by 2026. At that level, debt held by the public, measured as a percentage of GDP, would be more than twice the average over the past five decades (see figure below). Beyond the 10-year period, if current laws remained in place, the pressures that contributed to rising deficits during the baseline period would accelerate and push up debt even more sharply. Three decades from now, for instance, debt held by the public is projected to be about twice as high, relative to GDP, as it is this year — which would be higher than the United States has ever recorded.

Such high and rising debt would have serious negative consequences for the budget and the nation:

Federal spending on interest payments would increase substantially as a result of increases in interest rates, such as those projected to occur over the next few years.

Because federal borrowing reduces total saving in the economy, the nation’s capital stock would ultimately be smaller, and productivity and total wages would be lower.

Lawmakers would have less flexibility to use tax and spending policies to respond to unexpected challenges.

The likelihood of a fiscal crisis in the United States would increase. There would be a greater risk that investors would become unwilling to finance the government’s borrowing needs unless they were compensated with very high interest rates; if that happened, interest rates on federal debt would rise suddenly and sharply.

The Projected Deficit for 2016 Is Larger Than CBO’s March Estimate, but the 10-Year Deficit Is Below Previous Projections

The deficit that CBO now projects for 2016 is $56 billion larger than the amount the agency estimated in March. Revenues and outlays are both expected to be lower: revenues by $87 billion, mostly as a result of lower collections of individual and corporate income taxes, and outlays by $31 billion.

For the 2017–2026 period, CBO now projects a cumulative deficit that is $0.7 trillion smaller than the $9.3 trillion the agency previously projected. The average deficit in the baseline over the 2017–2026 period is 3.8 percent of GDP, compared with the 4.0 percent CBO projected in March.

That decrease stems primarily from revisions to CBO’s economic forecast. Projected revenues over the 10-year period are $0.4 trillion (1 percent) lower, in large part because of lower projected nominal GDP. However, projected outlays are lower by much more — $1.1 trillion (2 percent) — mainly because CBO anticipates lower interest rates, and thus smaller interest payments, than it did in March.

By 2026, debt held by the public is projected to total $23 trillion, whereas in March it was projected to total $24 trillion. Because CBO also lowered its projection of GDP for that year, both of those amounts equal 86 percent of GDP.

Economic Growth and Interest Rates Are Projected to Increase in the Near Term but Remain Lower Than in Earlier Decades

According to CBO’s projections, the economic expansion over the next two years will reduce the quantity of underused resources, or “slack,” in the economy. In addition, interest rates on federal borrowing are expected to rise over the next few years. Beyond the next two years, the economy is expected to grow more slowly.

Economic Growth

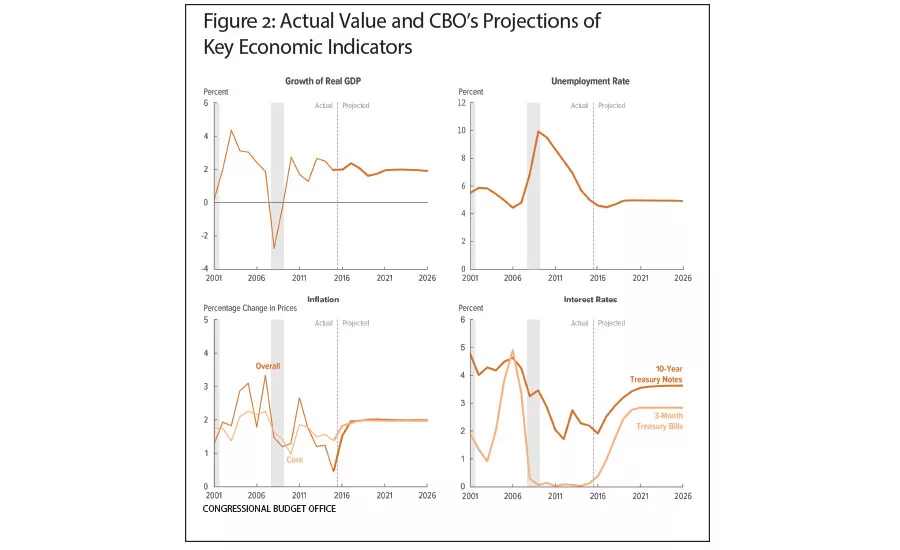

In real terms (that is, with adjustments to exclude the effects of inflation), GDP rose at an annual rate of 1.0 percent in the first half of calendar year 2016. However, CBO expects that the economy will expand more rapidly in the coming months, with GDP growing by 2.0 percent over the whole of 2016 and by 2.4 percent in 2017 — mainly because the major forces restraining the growth of investment, such as a decline in oil prices, have begun to subside (see figure below). Economic growth is expected to slow in 2018 and fall below but remain close to the growth of potential (maximum sustainable) GDP in 2019 and 2020. Most of the growth in output during the coming years will be driven by consumers, businesses, and home builders, CBO anticipates.

CBO’s projections for the second half of the 10-year period are not based on forecasts of cyclical developments in the economy; rather, they are based on the projected trends of underlying factors, such as growth in the labor force, the number of hours worked, and productivity. According to those projections, productivity will grow faster than it did over the past decade, and both actual and potential GDP will expand at an average annual rate of about 2 percent. However, that rate represents a significant slowdown from the average growth in potential output that occurred during the 1980s, 1990s, and early 2000s — mainly because of slower projected growth in the nation’s supply of labor, which is largely attributable to the ongoing retirement of baby boomers and the relatively stable labor force participation rate among working-age women.

Interest Rates

Because of slow economic growth in the first half of the year and increased uncertainty about global economic growth and financial stability, CBO expects the Federal Reserve to hold the target range for the federal funds rate at 0.25 percent to 0.5 percent until the fourth quarter of 2016. (The federal funds rate is the interest rate that financial institutions charge one another for overnight loans of their monetary reserves.) CBO anticipates that the central bank will gradually reduce the extent to which monetary policy supports economic growth, and, as a result, the federal funds rate will rise to 1.8 percent in the fourth quarter of 2018 and average 3.1 percent during the 2021–2026 period.

Interest rates on federal borrowing will also increase gradually over the next few years, CBO projects, as slack in the economy continues to diminish, inflation returns to the Federal Reserve’s 2 percent target, and the federal funds rate rises. For example, CBO projects that the interest rate on 10-year Treasury notes will be 1.9 percent in the fourth quarter of 2016, rise to 3.4 percent in the fourth quarter of 2020, and average 3.6 percent over the 2021–2026 period. That projected rise in interest rates reflects the expectation that both foreign and domestic economic growth will improve, which should result in higher interest rates abroad as well as in the United States. In addition, CBO expects the “term premium” — the extra return paid to bondholders for risk associated with holding long-term Treasury securities — to increase from historically low levels. In CBO’s estimation, the term premium has remained low, in part, because of low foreign interest rates, heightened concern about global economic growth, and increased demand for Treasury securities as a hedge against possible adverse economic outcomes.

Although CBO projects that interest rates will rise above those currently in effect, they would still be lower than the average rates during the 25-year period that preceded the most recent recession for several reasons: slower growth in the labor force, slightly slower growth in productivity, and only partial dissipation of the factors that have held down the term premium and increased the demand for Treasury securities.

The Labor Market

According to CBO’s estimates, the growth in output will heighten demand for labor over the next year and a half, leading to solid employment gains and eliminating labor market slack in 2017, thereby putting upward pressure on wages. The agency projects that the unemployment rate will fall below the estimated natural rate of unemployment (the rate that arises from all sources except fluctuations in the overall demand for goods and services), bottoming out at 4.5 percent in the fourth quarter of 2017. In CBO’s projections for later years, which are primarily based on long-term trends, the unemployment rate rises to 4.9 percent.

The increases in employment and wages in the near term are expected to mitigate an otherwise prevailing decline in participation in the labor force — both by encouraging people who were out of the labor force because of weak job prospects to enter it and by encouraging people who were considering leaving the labor force to remain in it. As a result, CBO anticipates that over the next year and a half, the rate of labor force participation will change little from the 62.7 percent that it was in the second quarter of this year. (The labor force participation rate is the percentage of people in the civilian noninstitutionalized population who are at least 16 years old and are either working or seeking work.) It is projected to decline by roughly 2½ percentage points through 2026.

The prevailing decline in the labor force participation rate reflects underlying demographic trends and, to a smaller degree, federal policies. More specifically, the factors that contribute to that decline include the continued retirement of baby boomers, reduced participation by less-skilled workers, and the lingering effects of the recession and weak recovery. In addition, certain aspects of federal laws, including provisions of the Affordable Care Act and the structure of the tax code, will reduce participation in the labor force by reducing people’s incentive to work or seek work.

Inflation

CBO expects that the diminishing slack in the economy, along with higher prices for crude oil, will put upward pressure on prices for goods and services. That upward pressure will be somewhat alleviated by the effects of a strong dollar in relation to other currencies. This year, CBO projects, the rate of inflation in the price index for personal consumption expenditures will rise to 1.5 percent from 0.5 percent in 2015. In 2017, the rate of inflation is projected to rise to the Federal Reserve’s longer-run goal of 2.0 percent; in CBO’s projections, it remains at that rate throughout the coming decade.

GDP and Interest Rates Are Now Projected to Be Lower Than CBO Estimated in January

CBO’s current economic projections differ in two important respects from those the agency made in January 2016. First, potential and actual real GDP are lower: By 2026, those measures are 1.6 percent lower than CBO previously projected. Second, interest rates are significantly lower than CBO projected in January. By 2026, short-term rates are 0.4 percentage points lower, and long-term rates are 0.5 percentage points lower. Other changes to CBO’s projections are more modest.

CBO now projects slower growth in real GDP for 2016, largely because growth during the first half of the year was weaker than previously anticipated. Downward revisions to potential and actual GDP over the decade were made on the basis of new data and a reassessment of projected growth in the labor force and in potential total factor productivity in the nonfarm business sector. (Total factor productivity is the average real output per unit of combined labor and capital services.)

The weak growth so far this year, coupled with uncertainty about the effects of the United Kingdom’s vote to leave the European Union, leads CBO to anticipate that the Federal Reserve will raise the federal funds rate more slowly than was projected in January. As a result of that revision, and because of lower projected interest rates abroad, CBO has revised downward its projections for the interest rates on 3-month Treasury bills and 10-year Treasury notes over the next several years. The downward revision to interest rates over the rest of the decade primarily reflects greater expected demand for Treasury securities.

For more information, visit http://bit.ly/2bjMSkR.

Toms Note:

In our year-end forecast 2016, I have continued to present the latest updated figures from the nonpartisan Congressional Budget Office (CBO). You might disagree, and you might be skeptical given your political persuasion. Whatever your orientation is, however, it might be worth reviewing the official outlook to see how it fits into your company’s strategic planning.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!