HARDI Releases Benchmarking Reports and Information

Mid-Season Survey Reports Optimism, Unitary Study Provides Regional Data

HARDI has released two study reports in an effort to assist distributors in business planning and benchmarking. The first of the two is the fifth annual “Mid-Season HVAC Distributor Survey,” conducted in partnership with JP Morgan Equity Research. According to the study, “The normalization of the HVAC market is happening, with demand and consumer behavior approaching something closer to a medium-term trend line, inventories less lean and more in line with demand, while pricing is becoming incrementally harder to come by.”

C. Stephen Tusa, JP Morgan’s HVAC industry analyst, noted that a hint of optimism seems to be rubbing off on HARDI distributors and that more than half of survey respondents expect their revenues to improve by 5 to 10 percent.

“For the first time in our survey, more distributors expected repair activity to decline. That could be an indication of an unlocking of the pent-up demand from units that were fixed instead of replaced over the past few years,” he said. “Sales of condensing units and furnaces have been better than expected and SEER mix has also improved. There has been more system replacement and consumers are opting for more expensive systems.”

Tusa explained that some of this optimism could be explained by a slightly improved housing and construction market outlook. According to him, it took almost five years from the first quarter 2006 peak for the market to find a bottom.

“Confidence in a recovery was improving in the back half of 2012,” he said. “The 2013 forecast had a positive bias because the correction had been so deep and painful. At the time it was difficult to generate a great deal of confidence in an aggressive growth forecast, but that would have been more accurate.”

Other key items in the survey explored inventory and pricing, the commercial market, and pointed information on the residential repair/replace dynamics. Inventory and pricing is something that the survey noted was changing.

“Inventories are no longer lean and pricing is getting tougher,” stated the report. “Neither pricing nor inventories are make-or-break issues for near-term earnings, but both are incrementally negative and remain areas to watch.”

Looking for quick answers on air conditioning, heating and refrigeration topics? Try Ask ACHR NEWS, our new smart AI search tool. Ask ACHR NEWS

According to the survey report, the commercial sector is expected to remain steady without any upward inflection.

“There were no major surprises in the commercial responses, with the tone slightly better but still pointing to average growth that struggles to move beyond the low-mid single-digit range,” noted the report.

This note was tempered with the fact that the survey focuses on unitary equipment sold through distribution and not the larger applied systems.

As for the residential demand environment, the survey reported that on overall second-quarter demand, roughly 70 percent of respondents saw increases in sales versus 30 percent seeing declines. The responses in regards to the repair/replace dynamic showed incremental progress matching the more upbeat assessment of the economy, according to

the report.

“The high single-digit growth we forecast in 2014 reflects a modestly higher replacement rate, and if the economy continues to improve then more improvement could come from housing completions,” said Tusa. “Replacement rates are the wild card. They could easily turn down, but the industry has some momentum at this point.”

The full report and accompanying webinar is now available for member and non-member purchase on HARDI’s website.

Q2 Unitary Market Share

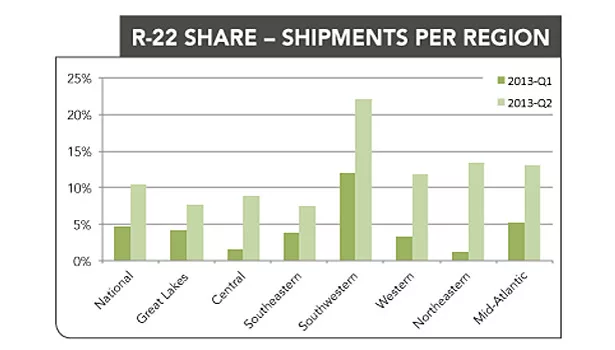

Another report released by the association is the second quarter “HARDI Unitary HVAC Market Share Report.” Compiled from HARDI distributor member participants, this report provides market share details regarding unitary sales by U.S. region, efficiency levels, and refrigerant type for both ducted and ductless cooling equipment, as well as furnaces and boilers. Over 2,000 branches nationwide are represented in the results. According to the report, 13-13.99 SEER was the most distributed for ducted unitary equipment nationally, but for ductless equipment, the most distributed efficiency rate was 18-18.99. The report further breaks out unitary equipment into multiple ducted and ductless categories, such as air conditioners and heat pumps. It also shows that ducted equipment distribution still remains the dominant equipment choice over ductless, but noted that when it comes to refrigerant, that R-410A was the top distributed. The report also breaks this information down into regions.

According to a press release about the unitary study from HARDI, the demand for R-22 dry-shipped units has been what it calls, “perplexing.”

“It is especially difficult when the performance can be so volatile from month-to-month,” noted the release. “HARDI distributors participating in this report have actual insight into the level of activity.”

The study is conducted in partnership with Better Data, a service of D&R International Ltd., and overseen by Toby Swope, manager of data analysis, D&R International, and Brian Loftus, market research and benchmarking analysis, HARDI. Participants do not receive financial compensation in exchange for their data, however, they do receive a copy of the quarterly report along with a detailed analysis of their own unitary results.

“Participants report that the monthly data collection process is very simple and accomplished in minutes,” said Swope. “This report is providing insight that is not available anywhere else.”

For more information on participating in the “HARDI Unitary HVAC Market Share Report,” visit www.hardinet.org/benchmarking.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!