EU Retailers Lagging HFC Targets

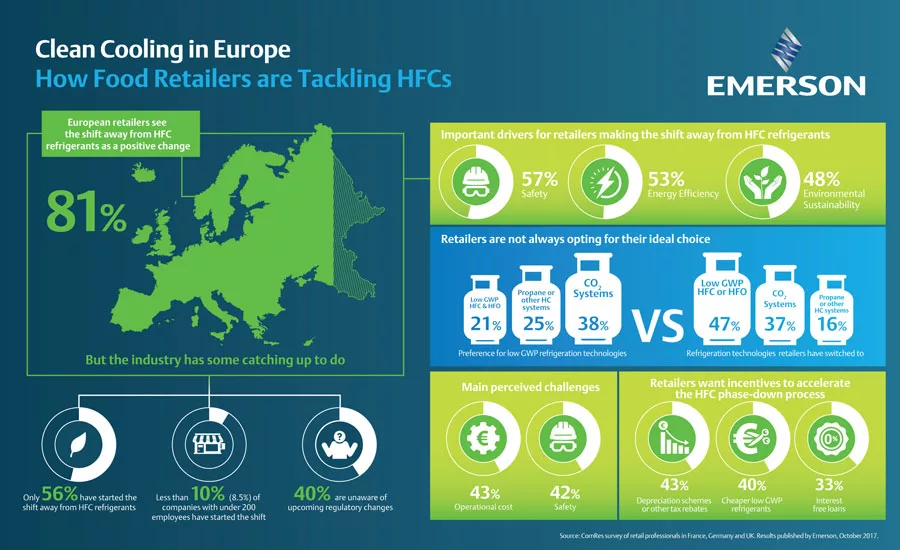

A LONG ROAD: Results from a recent survey of retailers’ perceptions of the European Union’s hydrofluorocarbon (HFC) phasedown. Although 86 percent see the shift away from HFCs as a positive, only 56 percent have started the process. Graphic courtesy of Emerson

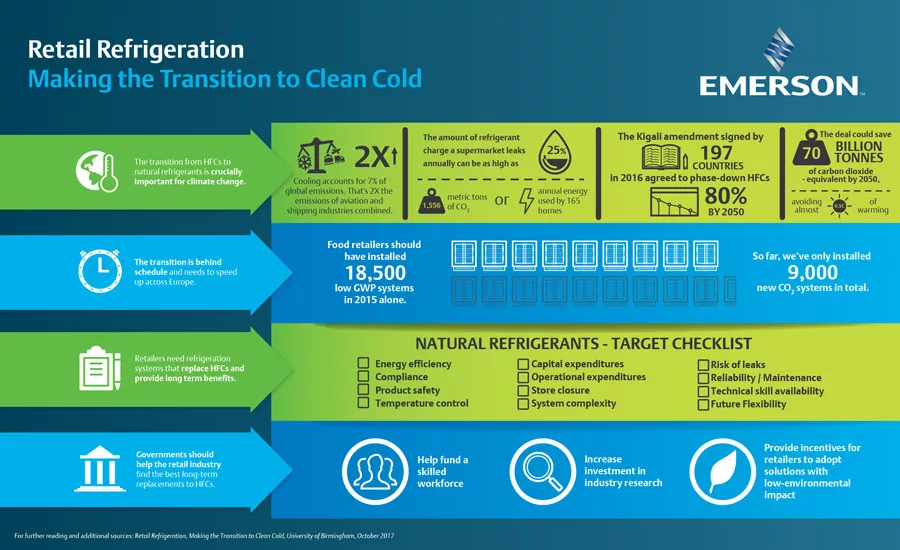

MAKING THE TRANSITION: Retailers in the EU are moving to natural refrigerants more quickly than their counterparts in the U.S. but not quickly enough to keep up with the EU’s aggressive F-gas Regulation. Graphic courtesy of Emerson

Supermarket retailers in the European Union (EU) are lagging behind the aggressive phasedown schedule for hydrofluorocarbons (HFCs) set by the EU’s F-gas Regulation, but the need to move swiftly to meet refrigerant targets should not eclipse the opportunities to address whole-system impacts of refrigeration. In addition, governments can play a key role in encouraging the transition to low-global warming potential (GWP) refrigerants and ensuring the solutions adopted deliver maximum long-term benefit.

Those were among the findings of the report, Retail Refrigeration: Making the Transition to Clean Cold, which examines what the move to natural refrigerants means for retailers and offers recommendations for the path forward. The report, from University of Birmingham’s Birmingham Energy Institute, was commissioned by Emerson Climate Technologies to coincide with the one-year anniversary of the Kigali Amendment to the Montreal Protocol.

The report focuses mainly on transitioning to natural refrigerants and hydrocarbons (HCs), stating: “A persistent concern among end users is that HFOs [hydrofluroolefins] remain vulnerable to future regulatory tightening.”

The report noted the F-gas Regulation will reduce the EU’s supply of HFCs by almost 80 percent by 2030. The phasedown trajectory is steep — in 2018, the HFC supply will effectively fall to 48 percent below its 2015 level.

“[The F-gas phasedown] gives food retailers a sharp incentive to replace F-gases with natural refrigerants,” the report states, “but it only tackles part of the problem — 75 percent of cooling emissions come from energy consumption rather than refrigerant leaks. Since the ultimate goal is zero-net-energy supermarkets, phasing out HFCs can only be the first step. Broaden the agenda, however, and supermarkets have a once-in-a-lifetime opportunity to develop refrigeration strategies that simultaneously advance business and environmental goals.”

The author of the report, Toby Peters, engineering and physical sciences professor in cold economy at the University of Birmingham, said the report highlights the need for the refrigeration industry, and retailers in particular, to consider the holistic, long-term impact of their technological choices.

“The phaseout of HFCs provides a unique opportunity to look beyond the choice of refrigerant and to fundamentally rethink store and system architectures,” Peters said. “Refrigeration systems introduced today could still be operating in 15 years’ time, and it’s imperative that we grasp the once-in-a-generation chance to deliver genuinely clean cold.”

Looking for quick answers on air conditioning, heating and refrigeration topics? Try Ask ACHR NEWS, our new smart AI search tool. Ask ACHR NEWS

The aggressive phasedown schedule of HFCs presents both a challenge and an opportunity for the retail industry, according to Eric Winandy, director of integrated solutions, Emerson Commercial and Residential Solutions.

“Although there is certainly pressure for retailers to act quickly, we must be careful not to rush into choosing new refrigeration systems, which eliminate HFCs but miss the opportunity to maximize energy efficiency and other long-term environmental benefits,” he said. “After all, improved energy efficiency equates to tangible cost savings and improved profitability, so making the right environmental choice can also deliver multimillion-euro savings for retailers across Europe.”

According to the report, European governments have a critical role to play in encouraging retailers to transition to natural refrigerants and ensure the solutions adopted deliver maximum long-term benefit. It recommends that governments:

- Invest significantly more into research and development of sustainable refrigeration and energy systems;

- Support the development of a clear pathway for sustainable refrigeration, not just low-GWP refrigerants;

- Provide incentives, not just penalties, for end users to accelerate the transition to low-impact systems. They should, for example, consider increasing depreciation allowances for investments in new refrigeration systems that are both low-GWP and demonstrably produce the best energy efficiency outcome for the proposed location; and

- Invest in the skills required to support the long-term transition to natural refrigerants, recognizing that an expanded workforce, with new competencies and certifications, is going to be required.

DIFFERENT EXPERIENCES

Are there lessons for U.S. retailers in the EU’s ongoing experience? Perhaps, but the EU’s experience with natural refrigerants was and is significantly different than the experience in the U.S., noted Danielle Wright, executive director, the North American Sustainable Refrigeration Council (NASRC).

“Stringent F-Gas regulations, heavy taxes on HFC refrigerants, and quicker updates when it comes to codes and standards drove the accelerated adoption of naturals in the EU when compared to the U.S.,” Wright said. “The U.S. faces challenges when it comes to first cost of systems and equipment, availability of trained technicians, and outdated safety standards and building codes. These are the hurdles the NASRC is working to address.”

Keilly Witman, owner, KW Refrigerant Management Strategy, said much of the EU’s report states the obvious.

“To pronounce that retailers need to take energy efficiency, operational concerns, and cost factors into account when phasing out various harmful refrigerants is stating what the [U.S.] Environmental Protection Agency’s [EPA’s} GreenChill Partnership advised from the time it began in 2007,” Witman told The NEWS. “And frankly, I felt in 2007 that we were expressing something that was already universally understood.”

Witman noted U.S. supermarkets choose refrigerants and refrigeration systems based on the business case for those products, which tends to eliminate choices that increase energy use, increase operational complexity, and increase life-cycle costs.

“I don’t think we need government help to point that out to anyone,” Witman said. “Of course, if governments here want to give retailers monetary incentives to overcome some of the hurdles that exist until new natural refrigerant technologies achieve economies of scale, I’m sure no one would say, ‘no,’ to free money.”

LESSONS LEARNED FROM THE EU

Retailers in Europe may be lagging behind the aggressive goals set by the F-gas regulations, but they are still well ahead of their counterparts in the U.S., noted Aaron Daly, global energy coordinator, Whole Foods Market Inc.

“They’re trying to move at a much swifter pace [in Europe] than we are, and I think the reality on the ground is they actually are moving faster,” Daly said. ”However, as it relates to the speed they need to move at to meet the regulatory requirements, it would seem as if they’re doing no better than we are.”

Daly added the European refrigeration market has been at work on the adoption of low-GWP and natural refrigerants longer than the U.S. has and, therefore, has a considerably higher number of store-based systems in place. Part of the credit for that, he said, goes to the clarity of their regulations — something that is not always the case here.

“In the U.S., there’s a lot of misunderstanding about where things are ultimately headed, and that leads to very mixed results,” he said. “There’s a lack of clarity about the ultimate intent of the refrigerant regulations, so the U.S. retail industry focuses, instead, on pressing issues, such as the competitive landscape and the changing retail environment, and only addresses refrigerant management issues when they become pain points.”

Daly said lessons the U.S. can learn from the European experience to date include not only technological solutions but also the importance of communication and training. On the technology side, the U.S. can benefit by not repeating mistakes made along the way in Europe.

“The appetite for risk in the retail industry is low, so when a mistake is made with a new technology, it sets everybody back as far as adoption,” he noted. “No one wants to pay the price for mistakes, and we have the luxury of learning from our European counterparts in that regard.”

As for communication and training, Daly credits associations such as the California Air Resources Board (CARB), the Food Marketing Institute (FMI), and the NASRC for creating an industry dialogue not only around technology but also policy.

“Refrigerant regulations in the U.S. seem to be in a constant state of flux, and, quite frankly, it can be difficult to determine where everything is eventually going to land,” Daly noted. “Although we don’t get much direction from the federal government or from most of the states, the refrigeration industry is doing a decent job of communication internally. That’s very helpful, particularly when the communication takes place in a way that gets down to the individual retailers.”

According to the University of Birmingham’s report, regardless of the demands of recent regulatory changes in the EU and U.S., supermarkets must focus not only on their choice of refrigerant but also on a broader set of criteria to make progress towards zero-net-energy supermarkets. These include total thermal demand, total system energy efficiency, preventing refrigerant leakage, maintenance, and decommissioning and end-of-life disposal.

“If supermarkets do adopt this approach, they can materially help to meet societal needs, support sustainable communities, improve energy efficiency, and combat climate change,” the report concluded.

Publication date: 1/8/2017

Want more HVAC industry news and information? Join The NEWS on Facebook, Twitter, and LinkedIn today!

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!