A Lack of Business Knowledge Often Leads to Failure

Business terms and concepts to understand to operate profitably

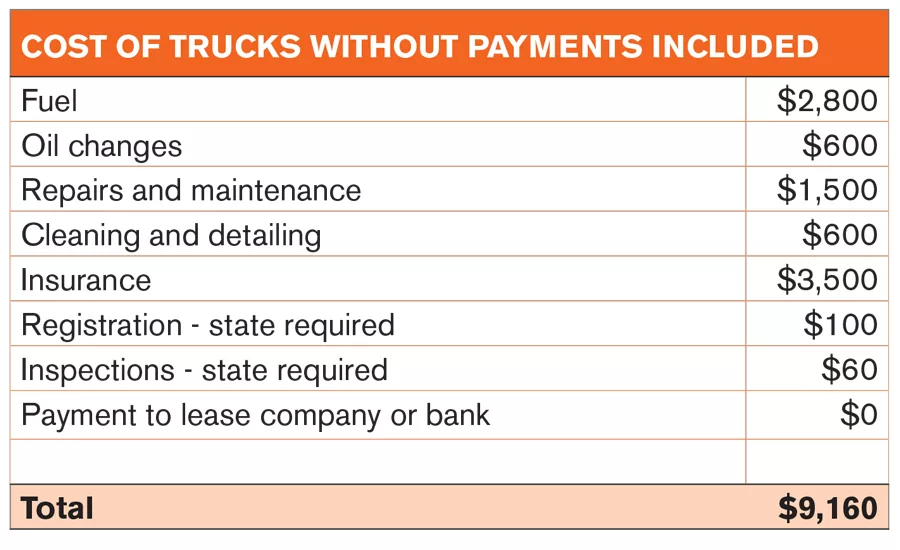

TABLE 1: This table showcases the cost of operating a truck without the payment of the truck included.

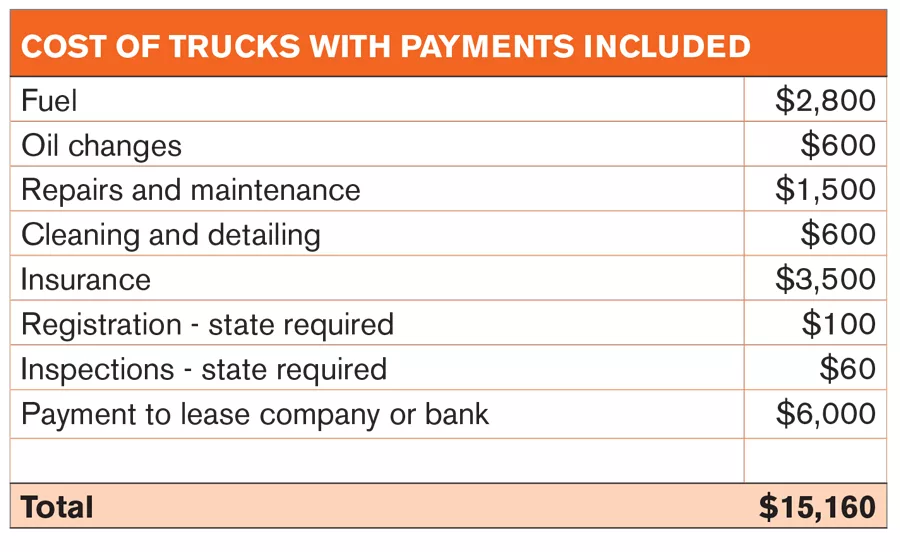

TABLE 2: This table showcases the cost of operating a truck with the payment of the truck included.

The high failure rate or inability to grow beyond a few trucks is due primarily to an entrepreneur’s lack of business training. The technical skills acquired, which are, of course, an asset, soon become a liability in terms of not having mastered business skills necessary for success and profitability.

To operate a profitable business, you must know more than metrics, such as bank account balances, accounts receivables, and payables.

Here are a few simple terms to understand:

- Gross Margin — This is how much money you have left over after all direct costs needed to perform the job or project. It is generally expressed as a dollar amount and percentage. It can be calculated by job or by a compilation of jobs, which is all jobs performed in say a month’s period.

- Profit and Loss Statement — This is your report card. If properly setup, it should confirm what you already know about your performance in each period. It is historical in nature, meaning the transactions on it have already occurred. A well-run company should receive this report card monthly. Other reports can be setup to provide granular information for real-time analysis.

- Budget — This is your roadmap. It is vital to know where you are in terms of hitting target sales goals and profitability as the year progresses. It can easily be adjusted as circumstances warrant.

TOP 10 CONCEPTS

Here are the top 10 concepts to become familiar with:

- Calculating true direct costs for labor and field service trucks;

- Determining a selling price and resulting gross margin for labor and field service trucks;

- Determining selling price for materials and equipment;

- Testing proposed selling prices against the near universe of competition;

- Determining sales required to support a given overhead;

- Calculating costs per man day and overhead burden;

- Calculating capacity to determine the number of field laborers required to achieve desired sales goals;

- Tracking bids and backlog to achieve accurate performance in measuring effectiveness of advertising dollars spent and performance of sold jobs;

- Tracking individual performance of field service technicians not job costing; and

- Utilizing this information in relation to competitor pricing.

CHECK THE PRICE TAG

The No. 1 rule in business: Don’t sell anything unless you know what it costs. Otherwise, you may be giving it away.

To arrive at a selling price, accurately determine your costs for labor and service vehicles.

Listed below are the required inputs to calculate direct labor cost and a method to calculate truck cost per hour:

Calculating Cost of Labor — You must accurately calculate a cost per man hour. This is not just the straight dollar rate you pay your technicians but a blended rate of all your technician’s pay plus all legally required obligations, such as employers contribution for Social Security and Medicare, working workman's compensation (WC), federal unemployment tax act (FUTA), state unemployment tax act (SUTA), local payroll taxes, and, if applicable, union benefits. It also includes other forms of compensation, such as paid holidays, paid time off (PTO), sick time, and inefficiency.

Looking for quick answers on air conditioning, heating and refrigeration topics? Try Ask ACHR NEWS, our new smart AI search tool. Ask ACHR NEWS

Calculating Cost of Field Service Vehicles — Often, companies include the cost or payment of the service truck in this calculation. This is a tactical error. You should only include costs that will be incurred by other competitors. These include insurance, fuel, oil changes, state inspection and registration, tires, and an estimate for repairs and maintenance. The payment of the truck should be an expense below your operating profit. Why? Because if a competitor has a fleet of trucks that are paid off, you may put yourself at a selling price disadvantage by including the monthly payment price of the truck in your cost.

Tables 1 and 2 compare and contrast the costs of operating a truck with and without the payment of the truck included.

The total cost in Table 1 is only $9,160. The $9,160 divided by 1,625 working hours per year results in a cost per hour of only $5.64. To achieve the same 55 percent gross margin, our sell price per hour is only $12.52.

Now, let’s see what happens when we add the truck payment yo the cost and its impact on selling price per hour.

Table 2 totals $15,160 per truck, including the $6,000 payment. If we simply divide the $15,160 by say 1,625 working hours in a year, the cost per hour for our truck is $ 9.33 per hour. If we want to achieve say a 55 percent gross margin on this cost, we would calculate by dividing $9.33 by the reciprocal of 55 percent. So, $9.33 divided by 0.45 equals a $20.73 per hour sell price.

This is quite a difference.

So, how do we recapture the cost of the purchase price of the truck? Not by increasing your selling price per hour, which makes you uncompetitive, but in performing enough volume of work to achieve the proper amount of sales throughout the year and earning a healthy earnings before interest, taxes, depreciation, and amortization (EBITDA) profit.

If you understand this concept, you have a big leg up on your competition.

Once the above concepts are mastered, you can be on your way to running a profitable business with firm knowledge in your decision-making process to positively impact your financial performance and bottom-line profit.

Publication date: 10/2/201

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!