Association Announces Insurance Program

"Insurance is available from several different top A-rated insurance companies depending on the kind of work the company performs and the type of coverage they are seeking," said Charlie Wiles, executive director of the American Indoor Air Quality Council. "Certification through the AmIAQ is required for program eligibility. Current members and certification holders of IAQA and IESO may also be eligible for this program."

The launch of this insurance program comes after months of work by IAQA, AmIAQ, and IESO officials in concert with Legends Environmental Insurance Services and other environmental insurance industry leaders. Through the beginning of February 2006, over 60 members of the AmIAQ/IAQA have attained insurance through this program, with an average savings of over 15 percent from their previous policy.

"In the past those companies who concentrated on microbial assessments and/or microbial remediation found insurance hard to come by," said Wiles. "If they found it, it was often at a cost that made the coverage inaccessible. This new program opens up access to insurance at an affordable price for those members of the IAQA-AmIAQ-IESO who perform up to 100 percent mold work."

Bill Lohman, president of Legends said that a lot of work went into creating the new program. "We worked on this project for quite some time," Lohman said. "In the end, the experience prerequisites, training requirements, due diligence, and attention to detail that the IAQA-AmIAQ-IESO has set for their certification holders enabled us to convince insurance underwriters that mold was not a four letter word, as long as the insured had appropriate American IAQ Council certification."

"They would not have done business with us without the insurance, regardless of how good our work product is," said Riera. She also mentioned that her company got four other jobs from another commercial office property manager when he heard her company was finally able to get insurance.

"We will make back the cost of the premium in less than one month," she said. "It was very nice to work with a company that uses such a great tool [online insurance certificate program] for delivering certificates to clients."

GETTING FEEDBACK FOR THE PROGRAM

Finding out what members want has been the key to the success of this program. Legends conducted a survey to see what insurance coverage members needed - and lacked.The survey results, summarized below by Wiles, can also be seen in Figures 1 through 4.

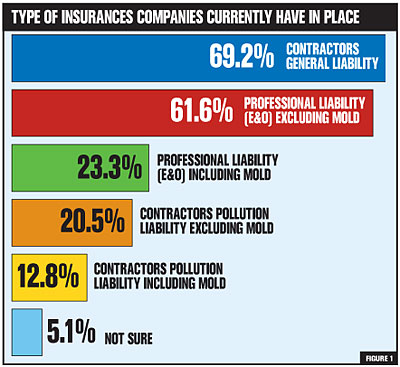

Result: More than 61 percent of the respondents have professional liability insurance excluding mold. (See figure 1.)

Looking for quick answers on air conditioning, heating and refrigeration topics? Try Ask ACHR NEWS, our new smart AI search tool. Ask ACHR NEWS

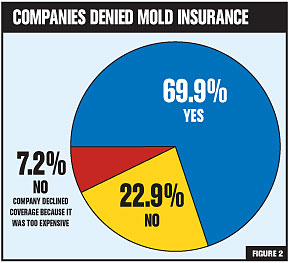

Results: At one time or another, 69.9 percent of the respondents were denied microbial coverage. Another 7.2 percent declined to purchase coverage because it was too expensive. (See figure 2.)

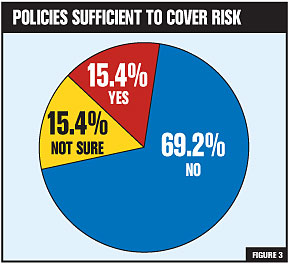

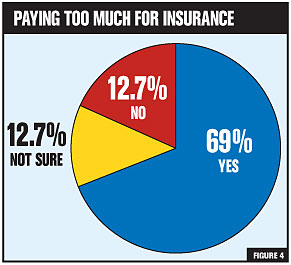

Results: Most feel that they are paying too much for insurance. This is reflective of the inadequacy of their policies and the high rates. (See figure 4.)

IAQA-AmIAQ-IESO encourages all members to take advantage of this insurance program.

For more information, visit www.iaqa.org, www.iaqcouncil.org, www.iestandards.org, and www.iaqa-marketing.com.

Sidebar: OSHA Vocabulary Test

To most people, an apron is a simple garment worn over the front of the body to protect one's clothes when cooking. But in the world of Occupational Safety and Health Administration (OSHA) regulations, a common term like apron can mean something else entirely. According to construction industry regulation 1926.606, under Subpart O: Motor Vehicles, Mechanized Equipment, and Marine Operations, an apron is "the area along the waterfront edge of the pier or wharf."Below you will find 10 common terms and their everyday definitions, and in a separate column, their very different OSHA definitions. Can you match the letter of the common term with the number of its OSHA definition? The OSHA definitions are taken from MANCOMM's OSHA Dictionary, a book containing all the terms and definitions from the 29 Code of Federal Regulations (CFR) OSHA parts 1903, 1904, 1910, and 1926 (Inspections, Recordkeeping, General Industry, and Construction).

If you get at least seven right, consider yourself exceptionally well versed in OSHA matters - and give yourself a pat on the back if you can cite the standards to which the OSHA definitions apply.

OSHA DEFINITIONS

1. A unit of lumber

2. A machine for cutting or grinding slabs and other coarse residue from the mill

3. A device used to serve as a warning for overhead objects

4. The nip point between any two inrunning rolls

5. A conducting connection, whether intentional or accidental, between an electrical circuit or equipment and the earth, or to some conducting body that serves in place of the earth

6. An intermittent motion imparted to the slide by momentary operation of the drive motor, after the clutch is engaged with the flywheel at rest

7. The effective length of an alloy steel chain sling measured from the top-bearing surface of the upper terminal component to the bottom-bearing surface of the lower terminal component

8. A head saw framework on a circular mill

9. A volume of 42 U.S. gallons

10. A lengthwise separation of wood, most of which occurs across the rings of annual growth

COMMON TERMS AND DEFINITIONS

A. Barrel: A large cylindrical container, usually made of wooden staves bound with hoops.

B. Bite: To cut, grip, or tear with the teeth.

C. Check: A written order to a bank to pay the specified amount.

D. Ground: Soil or land.

E. Hog: A domesticated pig.

F. Husk: The envelope of leaves around an ear of corn.

G. Jog: To run at a steady slow trot.

H. Package: A wrapped or boxed object.

I. Reach: To touch or grasp by stretching out or extending.

J. Telltale: One who informs on another; a tattler.

ANSWERS:

1) H; 2) E; 3) J; 4) B; 5) D; 6) G; 7) I; 8) F; 9) A; 10) C.

Publication date: 03/27/2006

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!