Economic Forecast Looks Solid

Total output for the country, as measured by gross domestic product (GDP), should increase by 3.6 percent in 2005. This is below the 4.4 percent growth seen in 2004, but it is still above the nation's long-term average growth rate. Recent price reports that show some upward pressure on prices will cause the Federal Reserve to continue to tighten the money supply by raising interest rates during 2005, contributing to the slowdown.

The housing market, which experienced a remarkable year in 2004, will see slightly reduced production in 2005, in part due to the higher levels of mortgage rates that will occur because of Federal Reserve policy. At the same time, the job market will continue to improve, adding strength to housing demand.

Total nonagricultural employment is expected to grow by 2 percent in 2005, as 2.6 million jobs are added to the economy.

Unfortunately, the negative effect of higher interest rates will more than offset the positive effect of stronger job growth. The result will be a decline in total housing starts of just over 4 percent in 2005.

Employment Growth Strengthens

The October employment report showed the strongest growth since March of this year. Total nonagricultural employment increased by 337,000, bringing total job gains during the first 10 months of 2004 to 2 million. Job growth is becoming more widespread, as employment increased in most major categories of employment in October.Manufacturing, which had performed miserably during the past three years, saw employment slip again in October. Despite this, employment in manufacturing is up so far in 2004, with gains in six of the 10 months of the year. This is especially good news for the areas of the country that have lagged due to their large manufacturing sectors.

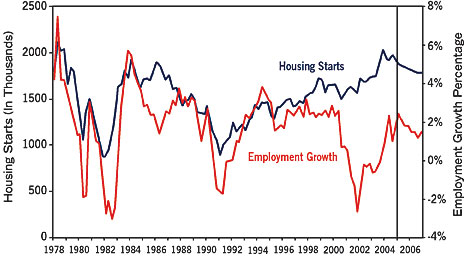

Housing To Weaken Despite Job Growth

The close tie of employment growth to housing demand has always been regarded as a "no brainer." That is, it is always assumed that strong employment growth leads to higher levels of housing demand. This occurs for a variety of reasons.First, a more robust job market leads to rising confidence among those who already are employed. Second, a growing job market gives new entrants to the labor force opportunities to gain employment and allows them to establish their own households - rental or owner-occupied. Third, a strong job market eventually leads to stronger wage gains, and adds to a household's ability to purchase housing.

As Figure 1 shows, however, this connection appears to have broken down during the past three years, as housing starts grew despite the significant loss in jobs across the economy. In fact, the real disconnect occurred during 2000 and 2001. Despite significant job losses, total housing production climbed.

Looking for quick answers on air conditioning, heating and refrigeration topics? Try Ask ACHR NEWS, our new smart AI search tool. Ask ACHR NEWS

As Figure 2 shows, the reason for the disconnect was significant decline in mortgage rates brought on by an aggressive Federal Re-serve policy that attempted to avoid and then cushion the recession. Since 2002, stronger job growth has been accompanied by rising housing starts.

Inflation Growth Concerns

The Federal Reserve has embarked on a path that will lead to higher interest rates during the next year. The federal funds rate, which had been held at just 1 percent in 2003, is expected to average 3 percent in 2005. Concern over an acceleration in the rate of inflation is motivating these actions.Recent data from the consumer and producer price reports appear to confirm that these concerns are justified. The Federal Reserve's actions will cause mortgage rates to rise during the next two years. Fixed-rate mortgages, which averaged 5.9 percent during the third quarter of 2003, will reach 6.9 percent by the end of 2005. Adjustable-rate mortgages will move from 4.1 percent to 5.6 percent during the same period.

Homeownership Limits

Although we may not like to do it, at times we must talk about the possibility of exhausting demand or running out of new consumers for housing. After all, there is a limit to how many new homes we need each year.Part of the support for the remarkable levels of new home construction that have occurred in the past few years has been an increase in the share of households that have chosen to own rather than to rent their homes. Figure 3 shows the increase in the homeownership rate that has occurred throughout the 1990s and into the first half of the current decade.

There is a limit to how high the homeownership rate will go. Several factors contribute to this limit.

First, there are some households that voluntarily choose to rent rather than own. These households may view their current location as temporary or they may rent simply because of convenience or their current family situation.

Second, some households are unable to save the down payment and other funds that would allow them to move into homeownership. Finally, the higher interest rates forecast during the next few years will simply make housing a bit less affordable.

So, the recent increase in the homeownership rate will actually limit the number of new home purchases during the next few years.

Declining Housing Starts In 2005

With rising mortgage rates, an economy that will be moving closer to trend growth, and job growth that will be modest, total housing starts in 2005 are expected to decline by 4.3 percent in 2005. This results in total housing starts that are almost equal to their value in 2003. The mix will be slightly different, however, as single-family housing starts at 1.527 million are expected to be a larger share of the total than they were in 2003.Stanley F. Duobinis, Ph.D., is president of Crystal Ball Economics Inc., Millersville, Md. He can be reached at 410-987-9623 or s.duobinis@att.net.

Publication date: 12/20/2004

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!