PRICE PERFORMANCE

Roller-coaster ride for aluminium prices

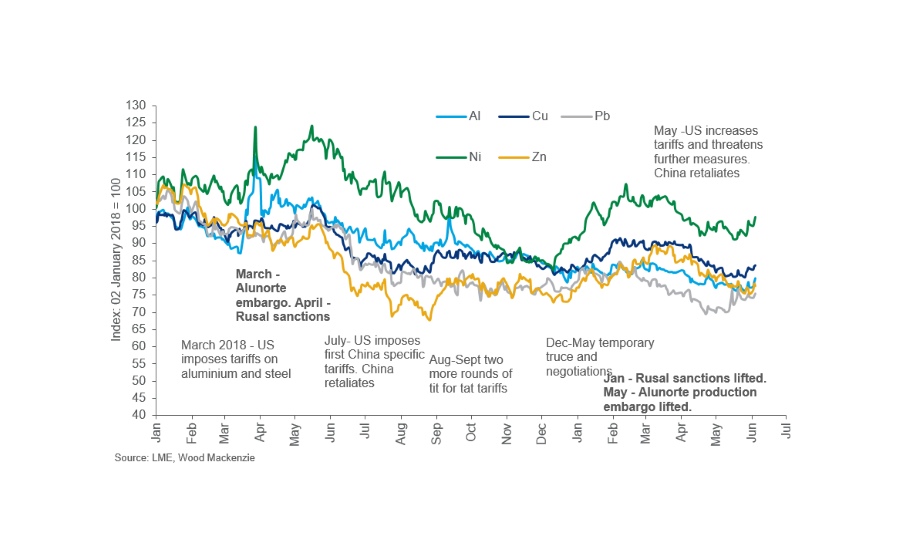

Last year was a tumultuous year for the aluminium industry. Sanctions on UC Rusal, Sections 232 tariffs and a production embargo on the Alunorte refinery left the market reeling. Overlaying this, sentiment was also hit by the escalation in the trade war between the US and China. Since the start of 2019 some of these disrupting factors have been removed, however, to say that the aluminium market has returned to ‘normality’ would be something of an understatement – the market remains far from ordinary and predictable.

Our global supply-demand balance points to a market in deficit this year. However, this aggregate calculation masks several negative micro dynamics for the aluminium market. Price performance on the LME has hardly been reflective of a market in deficit. Investor sentiment remains hostage to worries over the on-going US-China trade war and fears over a hard landing for the global economy. Escalating political tensions in the Middle East has added another layer to risk-off sentiment in the metals market.

Aluminium price hit by industry specific and wider policy driven events

China, often seen as a positive for the global economy, is struggling to kick-start. Key end-use sectors such as construction and transportation are weakening, while the trade war is dampening domestic consumption and investment. Outside China, primary aluminium consumption is under pressure. Weakness in demand has been amplified by record high Chinese semis exports which continue to arrive at a regular rate of 500 kt per month. China’s restrictions on imports of scrap is also weighing on primary aluminium consumption in the rest of the world. The use of scrap, in favor of primary, has been rising at semis operations in Europe, the US and Asia ex-China.

In the short-term market sentiment will remain subdued until there is a resolution to the trade war. However, we believe that the medium-term picture remains more optimistic.

There are considerable demand opportunities which are still to be fully realised in the use of aluminium within the automotive sector. We are already seeing the shift away from steel body sheet to aluminium in some mass-produced vehicles. However, the challenge for the industry will be to reduce auto body sheet production costs sufficiently, through innovation in rolling technology, to compete with advanced steels on a cost basis. The requirement to lightweight will be particularly important for typically heavy EVs, where aluminium is expected to make gains from lightweighting in body applications. A further upside is the development of new heat treatable alloys, which can be used for full battery enclosures.

Beside new demand avenues, aluminium will benefit from the traditional end-use sectors in Asia ex China. Rising income per capita, urbanization and positive demographic trends will support demand growth.

Despite short term headwinds, the outlook for aluminium market and the LME price remains positive. Slower demand growth but also slower output growth, so far, leaves our 2019 market balance in deficit. We expect this trend of market deficits to persist at least until 2023 as new production projects will remain few and far between.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!