How Mestek’s 2000 Acquisition of Met-Coil Ushered in the New Millennium and Industry Consolidation

As you know, SNIPS was gracious enough to select me as their ICON of the year for 2021. It was an honor. During my interviews with the Editor, Austin Keating, I reviewed with him the major events of the past half-century of HVAC development. I noticed that I had a direct hand in many of these major events – at least the first three decades; and that much of this development was neatly bookended by the decades. Hence, it seemed a good idea to tell these stories decade by decade.

When thinking about the 2000s, there is little, if anything, I had a direct hand in. However, as the new millennium opened, I was a marketing consultant to Met-Coil Systems, parent to both The Lockformer Company and Iowa Precision Industries (formerly Welty-Way Products). I was well-positioned to view major changes that would start in the early 2000s that continue today.

During the first decade of the new millennium, there was not much in the new machinery development, save Lockformer’s introduction of the first industry WaterJet for cutting ductliner and some “tweaking” of ductlines to make them more efficient. But there was industry consolidation, both with the major machinery manufacturers and wholesalers. So, let’s start on the machinery side with Mestek’s 2000 acquisition of Met-Coil.

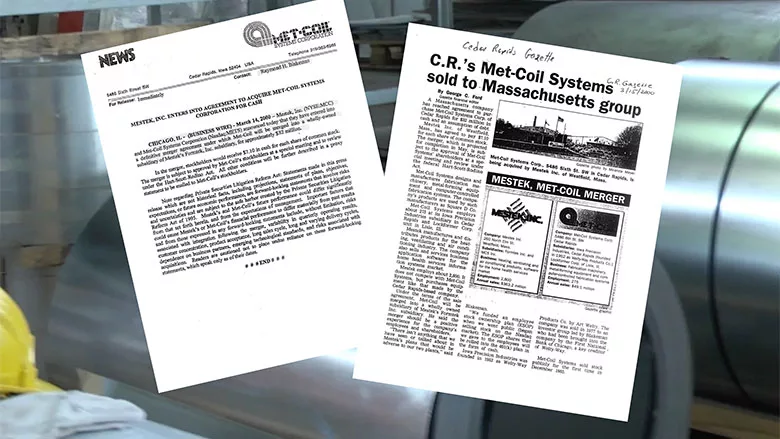

Met-Coil Systems was formed in the late ‘70s to acquire Welty-Way Products. It later added Lockformer and other companies, such as Roper-Whitney, now owned by Tennsmith, Mark One and Rowe. Headed by Ray Blakeman, he secured outside investors who by the late ‘90s wanted their investment back. With the “hot” construction market nationwide, and because of Ray’s long-term relationship with John Reed, CEO of Mestek; Mestek’s purchase of Rowe in 1996; and Mestek being a long-time user and fan of Lockformer’s roll-forming equipment, Ray approached John to see if he had interest. The brands fit in with Mestek’s other machinery companies. John agreed to purchase Met-Coil in 2000. However, there were clouds on the horizon – environmental clouds.

Due to solvent mishandling in the ‘60s and ‘70s at Lockformer’s Lisle, Illinois plant, the soil and groundwater south of the plant and in a downstream neighborhood were found to be environmentally non-compliant. Private lawsuits were filed, and federal and state enforcement actions undertaken. Lockformer had to pay for clean-up systems, pollution mitigation and private damages. That led to a bankruptcy filing in 2003, settled by creating a fund to finish the remediation and pay the claimants.

Enter St. Louis based Engel Industries, Lockformer and IPI’s biggest competitor. Through a series of “buy-outs” in the ‘90s, Engel was sold and re-sold. Not knowing the end results of the environmental bankruptcy filing for Lockformer, Mestek purchased Engel in late 2003 to protect the roll-forming product lines, which indirectly set the stage for Vicon’s move into full competition with today’s Mestek Machinery brands.

Market economies do not like vacuums, so regardless of how Mestek’s Engel acquisition played out, competitors were bound to come – leading to today’s Vicon and to a lesser degree, Precision Products Manufacturing International. Here’s how Avalon Machinery’s Vicon Plasma machine evolved into Vicon Machinery.

Competition among sheet metal machinery companies

After Mestek absorbed Engel and moved manufacturing out of the St. Louis area, by mid-decade, there were ex-Engel employees available for work and two important, long-time Engel rep firms with no machinery products to sell: Missouri-based Central States Machinery and Long Island based Walsh-Atkinson.

Engel used rep firms for most of its existence, as opposed to specialized HVAC machinery dealers that both Lockformer and IPI used. Some of Engel’s reps were one-man operations and some were major firms such as Central States and Walsh-Atkinson, which also handled Duro-Dyne’s pin-spotters, as many Engel rep firms did. Lockformer and IPI’s dealers were required to stock machinery, which would later play into Vicon’s hands.

In the first half of the ‘90s, I recapped the CTI patent lawsuits that put Vicon in the hands of Tim Walsh, President of Walsh-Atkinson. He formed Plasma Automation to purchase Avalon Machinery, parent of Vicon. Central States and Walsh-Atkinson teamed up to add a full machinery line to the Vicon Plasma table. Then viola: the company the industry knows today, Vicon Machinery, came into form. They manufactured in the St. Louis area, the pieces were already there and Vicon stitched it back together. By the 2007 Dallas AHR Show, Vicon had a full ductline to sell and the rest is history.

Next: The demise of Engel reps; Lockformer and IPI’s, and other machinery manufacturers’ dealer networks; and the national consolidation of local distributors that lead to large regional HVAC super-wholesalers.

The rise of direct dealers in the HVAC industry

When I recently reviewed my 1970 North American dealer map for Lockformer and Welty-Way, I noted it looks quite different today for the surviving brands under Mestek Machinery. While each company had their own distribution, they shared many. From that early 1970s map, the geography of the major North American markets was about 90% covered by dealers. The rest were “direct” markets. Today, that map is less than a third covered by dealers and about two-thirds direct, and growing. What happened?

After WWII and the Korean war, with the growth of air conditioning, as in many other industries, many returning veterans started companies; some specializing as HVAC machinery dealers to sell and service the growing sheet metal/air-conditioning industry – a few added supply lines. A couple of generations later, many of the offspring decided not to enter the family business and pursued other options. Partnerships broke up; and many just died off. The ones that did not, branched out as did the N. B. Handy Company and Gladwin Machinery, but Gladwin’s main line today is not HVAC. It is industrial.

In 1970, my Engel map shows almost exclusive single rep organizations. Not that a dealer network is better for sales than a rep firm – just a different road to market. Each has its advantages and disadvantages. But for the reasons above, these small, often one-man operations just died off – particularly after Mestek’s 2003 acquisition. However, by the late ‘90s, Engel was moving into distribution and much of that was due to, again, the early CTI lawsuit.

Ten years earlier, Ray Blakeman successfully navigated Lockformer through the CTI patent lawsuit, but the financial cost dented the balance sheet. Ironically, how Blakeman raised the cash post-lawsuit settlement would later help Vicon.

I mentioned in the first ‘90s section that Levine’s successful suit would upend the industry in many ways. Here’s another example. For Lockformer (Met-Coil) to pay the $15MM judgement, Ray Blakeman needed cash and he needed it fast. He had to sell off some assets, notably his Asia/Pacific dealers, but more importantly, was the change he made in his U. S. distribution dealer network. He went to his strongest dealers offering a 25% discount if they would agree to stock a significant amount of inventory and paying upfront – essentially setting up Master Dealers. His carrot to the dealers was to eliminate some by turning over their business and needs (think parts) to a Master Dealer. The mid-Atlantic is a perfect example.

In 1971 when I was working for Gripnail, I called N. B. Handy Company, based in Lynchburg, Virginia – started in 1891. They had only one outside branch, Roanoke. Handy was one of those machinery dealers that also sold HVAC supplies. By the mid-nineties, they had operations from South Florida to Northern Maryland.

Conklin Metals – started in 1874 – as with Handy was an old-line distributor with one branch operation in the 1970s before they moved outside their Atlanta base. Through generic growth and acquisitions, today they have branches throughout the Southeast and dominate the HVAC supply and machinery business.

Conklin was one of those Lockformer dealers that was cut for the new Master Dealer program. I’m sure you can guess the reaction when Conklin received Ray Blakeman’s letter (circa early to mid-90s) turning their long-time Lockformer business and relationship over to Handy. They, along with other IPI and Lockformer dealers, were not too pleased. That lead them to approach Engel, which Engel was all too happy to accept.

In 2003, Engel became part of Mestek, leaving quite a distribution mess in the industry for machinery. Within ten years, Vicon would enter the market and pick up many of these dealers. They were first Lockformer/IPI; then Engel; and now Vicon. Conklin was one and now gives Mestek Machinery a good run for their money. Who would have guessed!

Had Met-Coil not lost the CTI suit and had it not been for the Lockformer’s environmental bankruptcy filing, the HVAC machinery world would be quite different today. All machinery manufacturers to some degree are facing distribution issues today: Securing quality sales and service outlets or do it themselves. However, some old-line dealers have successfully navigated these seismic changes and are doing a good job: Handy, Gladwin, Hercules; and Conklin Metals come to mind, but not many others.

To a lesser degree, the same dynamics hold for the wholesale distributor. With the families who started HVAC distribution businesses, many offspring elected not to go into the family business, and this led to “selling out” when (or if) the right company came along. Some of these companies were “roll-up” acquisition wholesalers. A good example is the New England market.

I was not aware of Homans Associates in New England during the 1970s. When I returned to Ductmate in 1986 to head up sales and marketing, Homans was a Ward dealer along with supply distribution agreements with many of the companies that HVAC contractors rely on for their everyday needs: Ductmate; Duro-Dyne; Gripnail; Hardcast; and ductliner manufacturers.

Today Homans has multiple branches throughout the Northeast and a division of WATSCO, one of those roll-up distributors – publicly traded on the NYSE – that in addition to Homans, subsidiaries include: East Coast (acquired Three States Supply) with multiple branches throughout the Southeast; Baker-Coastline; and others.

Other old-line HVAC supply distributors have also grown, but have remained independent: MacArthur Co. of St. Paul, Minnesota; Gensco/Slakey Bros. (Northern and Southern West Coast, respectively); Denver based Hercules; American Metals, Springfield, Illinois; Conklin; and Handy until 2022. To my knowledge, only Hercules, Handy, Conklin, East Coast, and Lyon-Conklin out of Baltimore, a division of Ferguson, have both HVAC machinery and supply product lines.

The rise of the waterjet

As I’ve mentioned, I did not observe a lot of new machinery developments in the early 2000s. But the WaterJet is an exceptional exception. Developed by Lockformer – another first in a long line of sheet metal innovations over the years – waterjets cut fiberglass ductliner and other new duct lining products introduced to the market. Elastomerics for one.

The best way to describe the effect on the market is to repeat a story Mike Bailey, Mestek Machinery’s Sr. V. P. Sales & New Product Development, told to me when he pre-attended the January, 2001 Atlanta AHR Show. Mike was a sales rep for N. B. Handy. While the Met-Coil team was setting up the booth, Mike asked Rian Scheel “What was that” pointing to a machine that looked basically like a run-of-the-mill plasma cutter, but with an arched shaped tube running up over it. Rian replied, “a WaterJet.” Mike asked, “How much does it cost?” “Around $100,000.” Mike choked and said no one will ever pay that price. At the show’s opening, one of Mike’s local customers just asked: “How soon can I get one?” Two weeks after the show, he had multiple orders.

Today, a waterjet is a must have for any contractor cutting a significant amount of ductliner with many brands now on the market.

An additional trend during the decade was the growth of “fabricators,” companies that do not compete with other contractors who install ductwork. They build to order for other contractors to install – basically a duct manufacturer. The industry tried this in the ‘70s and ‘80s, with limited success due to the “structure” of the market. It didn’t take off until fab-only companies formed.

With my write-up of the 2010s, I will address this in more detail along with the trend to pre-assembled duct, or “manifold” duct – the process of fabricating and assembling as much duct in shop before sending to the field for hanging. Those topics, the use of BIM in drawing duct and the introduction of many new products that entered the market during this decade, will end my half-century commentary for SNIPS.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!