Steel tariffs may continue impacting sheet metal products

The White House decision to institute tariffs on most imports of steel and aluminum has impacted prices worldwide. Here’s why and what might come next

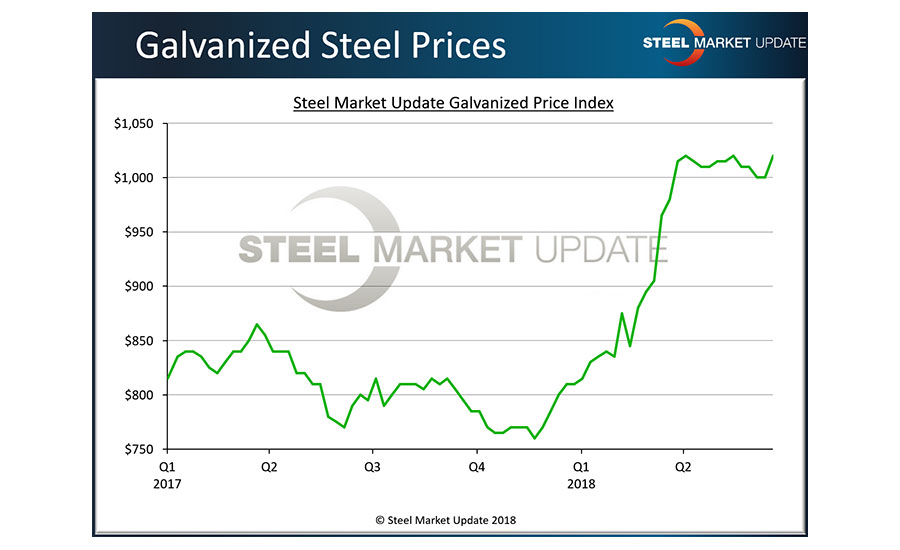

Steel prices in 2018 are up 60 percent from the market cycle’s low point set late last year, and they are likely to move even higher due to events on the trade front.

Were it not for persistently strong steel demand, including in the construction sector, the uncertainty caused by the Trump administration tariffs could be a much bigger issue for the market.

Flat-rolled steel prices, including galvanized steel used by mechanical contractors, are at levels not seen since 2008, and there is no sign of a reversal anytime soon. Why? Because this market is being controlled by the U.S. government and its desire to keep domestic steel production above 80 percent of capacity. What follows is some historical context.

U.S. steel producers have been lobbying hard for years for government intervention, claiming that predatory trade practices — and the dumping of steel by China and other nations — has decimated the U.S. steel industry. Globally, steelmakers produce about 1.7 billion tons of steel annually, half of it in China. What the Chinese economy cannot consume internally ends up on the world market, pushing global prices down, including prices in the United States as foreign steel floods its market. The fact that China can make steel, ship it halfway around the world and sell it in the U.S. more cheaply than domestic producers can only be explained by China’s state-subsidized mills routinely violating free-trade rules.

Officials with domestic steel mills say they believe decades of such unfair competition by China and other “bad actors” has contributed to a host of mergers and bankruptcies among American mills. Today, the industry is a fraction of its former size, with fewer than a dozen major steel companies in the United States employing fewer than 150,000 workers. With fewer mills, comes less domestic competition, and the better mills are able to control supply.

A changing market

The consolidation of the U.S. steel industry has not been all about unfair competition, however. Like all other industries, steel has evolved and the fittest have survived. Much of it can be attributed to huge leaps in productivity brought on by the growth of electric arc furnace steel production. More than half the steel produced in the U.S. today comes from “mini” mills, such as Nucor and Steel Dynamics, which produce it by re-melting steel scrap. Steel that used to take more than 10 man-hours per ton to produce can now be made in less than one. The streamlined U.S. steel industry is about as efficient and profitable today as it has ever been, which makes the current trade machinations seem that much more puzzling to many observers.

U.S. steel mills have fought against foreign steel flooding the domestic market by filing and winning numerous anti-dumping and countervailing duty cases against China and many other steel-exporting countries. Most recently, the steel mills filed a circumvention case against Vietnam and China as the mills claimed China was evading U.S. duty orders by first sending steel substrates to Vietnam.

The Vietnamese further processed the steel, shipping it to the United States as cold-rolled and galvanized steel. The U.S. Department of Commerce has ruled that such processing is no longer sufficient to change the steel’s country of origin. The domestic mills won that case and have now filed new circumvention cases against Korea and Taiwan.

“The precedent set under the Chinese orders, if followed, will allow orders on a few countries to be expanded indefinitely,” said Washington trade attorney Lewis Leibowitz. “The concept is dangerous to steel traders, importers and users in the United States. The Commerce Department’s determination in the China cases will certainly be challenged in the WTO (World Trade Organization), and the U.S. could well lose. A lot of damage will ensue before those decisions can be implemented, however.”

Tight supplies become tighter

These trade actions have helped to tighten supply and to push steel prices higher. However, these victories by the domestic mills are not the only reason steel prices are so high. Earlier this year, President Donald Trump invoked the seldom-used Section 232 of the Trade Expansion Act, a little-known 1962 law aimed at opening borders to U.S. goods, to enact the tariffs and protect the steel industry and its 150,000 jobs. A Commerce Department investigation subsequently determined that healthy steel and aluminum industries are essential to the nation’s security.

The administration levied tariffs of 25 percent on steel imports and 10 percent on aluminum imports, effective May 1.

Close allies Canada, Mexico and the 28 European Union nations were given temporary exemptions from the Section 232 tariffs. Apparently dissatisfied with the progress of North American Free Trade Agreement negotiations and other trade talks, Trump stunned many market observers by revoking the exemptions and hitting the United States’ closest trading partners, effective June 1, with the same tariffs faced by China and other questionable traders. China masks its exports to the United States by shipping them through other countries, the administration argued, so trade action is necessary on all nations to prevent such circumvention.

Not all the world’s countries are subject to the tariffs. The nations of Argentina, Brazil and South Korea negotiated quotas instead, which allow them to export only a percentage of their average shipments to the U.S. during the past three years. Experts warn that these three countries could hit their quota limits in the second half of 2018, at which point shipments would cease, contributing to a possible supply shortage late in the year.

Exemption battle

Facing the possibility they could be cut off from foreign sources, many manufacturers argued that they are dependent on imported materials that are not sufficiently available in the United States. So the Commerce Department established a product-exclusion process through which individual companies could request exemptions.

As of mid-June, department officials had been swamped by more than 20,000 exclusion requests for steel products and 2,500 exclusion requests for aluminum products, nearly four times more than originally anticipated. In testimony June 20 before the Senate Finance Committee, Commerce Secretary Wilbur Ross reported that the department had acted on just 98 requests for steel products, granting 42 and denying 56. To date, Steel Market Update is unaware of any galvanized products receiving exclusions.

Ross assured the committee that the department was conducting a fair, transparent and expeditious review process. But his assurances were met with skepticism. Sen. Ron Wyden (D-Ore.) was among the skeptics.

“It’s frustrating to watch as the administration’s trade moves seem more like knee-jerk impulses than any kind of carefully thought-out strategy,” Wyden said. “Its most obvious accomplishment on trade is sowing economic chaos that has united our allies and China against us.”

Will the Commerce Department deny exclusion requests if they were objected to by competitors? Will it approve requests that received no objections? The standard to be used is unclear, making it impossible to predict how the product review process will play out.

Are cars next?

Trump recently announced another Section 232 investigation, this time on imports of automobiles and auto parts. Using the same argument, the president contends competition from foreign automakers poses a threat to the viability of the domestic auto industry, and by extension the health of the U.S. economy and national security. A hearing was scheduled for July 19-20 in Washington, D.C., on proposed tariffs of 25 percent on auto imports. Perhaps no other industry has a more complex global supply chain than automotive, which is a big consumer of galvanized steel. Rather than returning auto production to the U.S., one study predicts such a move would cut U.S. production by 1.5 percent and cost American autoworkers 195,000 jobs.

In June, the Trump administration announced new tariffs on $50 billion in goods from China under Section 301 of the Trade Act of 1974, a law that gives the president wide latitude to fight unfair trade. The move is designed to protect the intellectual property of U.S. companies doing business in China. Not surprisingly, the Chinese have responded with more retaliatory tariffs on U.S. exports. Indeed, all the major trading nations hit with U.S. tariffs — including Canada, Mexico, the EU, Turkey and India — have announced retaliatory tariffs of comparable scale. While these trade conflicts extend well beyond steel to a host of agricultural and consumer goods, the brewing trade war has serious implications for all aspects of the U.S. economy.

Ever since the Section 232 investigations were announced last year, they have had an effect on the market. Some buyers have been reluctant to place foreign orders with long lead times for fear of what might happen before they receive product. With less foreign competition, domestic producers have pushed through a series of price hikes, raising prices dramatically.

Price impacts

Steel Market Update data shows the average price of hot-rolled coil as of June 18 at about $900 per ton with lead times on orders extended to four to eight weeks; cold-rolled coil at $1,015 per ton with lead times of five to nine weeks; 0.060-inch G-90 galvanized coil at $1,106 per ton with lead times of five to 12 weeks; and Galvalume 0.0142” AZ-50 Grade 80 coil at $1,316 with lead times of six weeks to two months. Steel Market Update’s Price Momentum Indicator is pointing higher as prices are expected to rise further over the next 30-60 days.

In light of the Trump administration’s moves, some U.S. producers have already begun to ramp up capacity. U.S. Steel is restarting two steel blast furnaces in Granite City, Ill. Republic Steel is restarting an idled electric arc furnace in Lorain, Ohio. Liberty Steel is reopening its wire rod coil steel facility in Georgetown, S.C. And India’s JSW Steel has announced a $500 million investment to acquire and upgrade the Acero Junction mill in Mingo Junction, Ohio. The U.S. Steel Corp. plant will have the most immediate impact on the flat-rolled market, adding about 2.5 million tons of new flat-rolled steel capacity. Last year, foreign mills shipped nearly 38 million tons into the American market. U.S. Steel’s new capacity falls well short of replacing potential missing foreign tonnage.

Instead of replacing foreign steel imports, many buyers have been paying the 25 percent duty to keep themselves supplied. This has helped to keep a floor on prices at much higher levels than what is available in the rest of the world.

Steel Market Update’s parent company, the CRU Group, indexes steel prices from around the world, and as of late June, hot rolled was being sold out of Asia for $560 per net ton and out of Europe at $545-$599 per net ton.

Winners and losers

Sources of supply are very much still in a state of flux, depending on buyers’ needs and locations. The tariffs will have the effect of picking winners and losers. One company whose future may be on the line is California Steel Industries, a West Coast re-roller that relies on imported slabs. A slab is a semi-finished product that is turned into hot-rolled sheet and then often processed into cold-rolled and galvanized steel. Other U.S. steelmakers have objected to CSI’s requests for exclusion from the tariffs, arguing that the slabs CSI requires can be made in the United States. The cost to transport the slabs from mills far to the east, which are unlikely to sell to a rival, make it impractical for CSI to source domestically, which puts the mill at a big competitive disadvantage.

What does all this mean to the HVAC and sheet metal industry? So far, the economy remains robust. Housing starts rose 5 percent in May to a seasonally adjusted annual rate of 1.35 million, the highest level since July 2007. But turmoil on the trade front could take a toll on U.S. gross domestic product growth. Galvanized steel prices are high and likely to go higher before the uncertainty shakes out. With imports into the U.S. restricted by tariffs and quotas, supplies could get tight later this year. Stay close to your suppliers. You may find yourself glad to get steel, regardless of what it costs.

For more information on tariffs and trade and the other trends affecting the construction/HVAC market, there’s still time to register for Steel Market Update’s annual Steel Summit Conference Aug. 27-29 in Atlanta at steelmarketupdate.com/events/steel-summit.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!